AngloGold Ashanti (AU) has been in steady decline since July’s $38 a share peak, down almost 45% in total after this week’s price dump in gold and silver. I believe the sell-off is getting a little overdone for one of the largest gold/silver/copper miners in the world.

For new investment capital, you can now buy AngloGold at the lowest forward-projected price-to-earnings valuation of the major global gold producers. On the upside, the company is generating record free cash flow today, has repaid most all of its debt, and still has reserves likely in the 10- to 15-year range at current metals pricing. If you are building out a precious metal portfolio, like I am, AngloGold deserves your consideration.

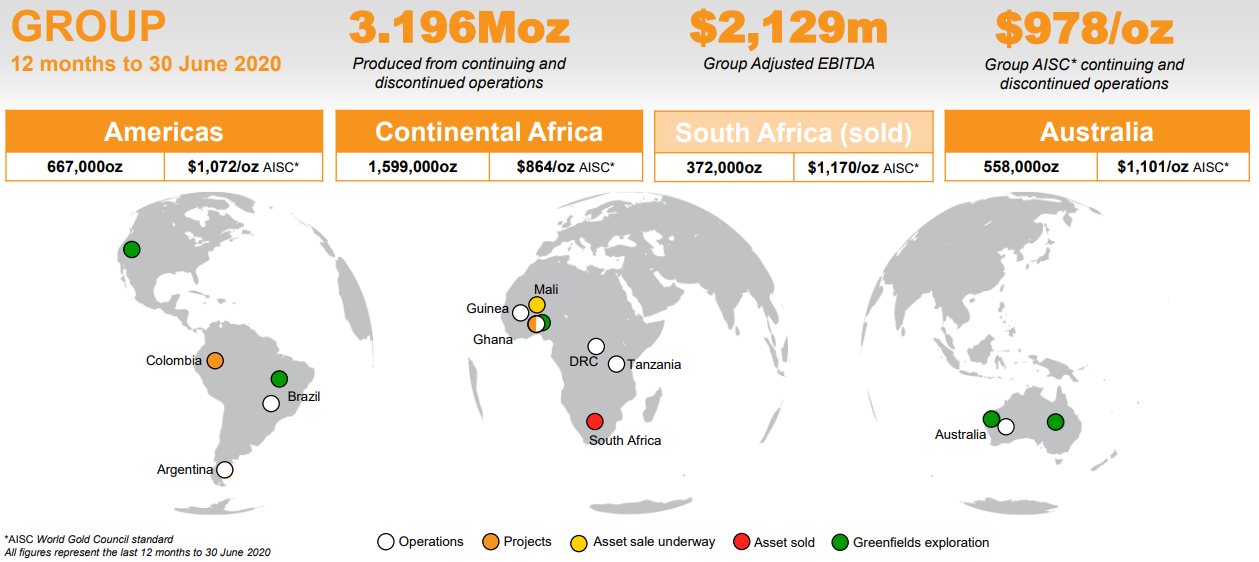

The company just exited its South African mine assets, the mainstay of revenue and cash flow generation several decades ago. The South Africa mines were sold to Harmony (HMY) in September for $300 million, representing 12% of trailing 12-month company production, and some of its highest all-in cost operations.

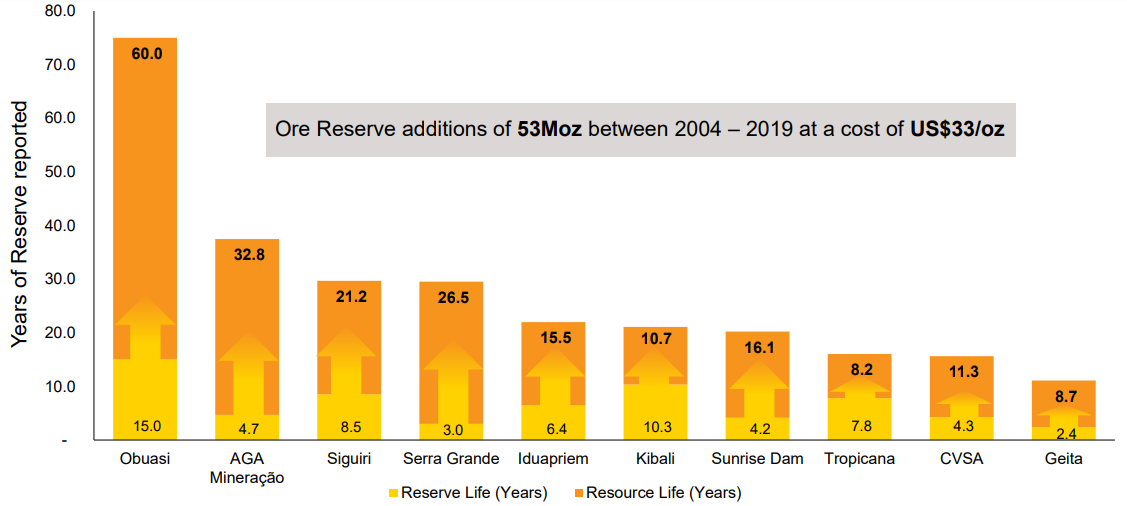

The remaining mine-life estimates of 2 years to 15 years, using proven ore reserves, are pictured below. The good news is, each asset has the ability and potential to pull new revenue and production out of the ground with higher gold prices, well above the conservative $1100 an ounce, long-term selling price assumptions of 2019 to value “economic” reserves.

Image Source: Company Presentation

AngloGold’s reserves and production come with extra mining “jurisdiction” risk, however. Less-stable African and South American mining jurisdictions and governments can pose future problems for your AU investment. Everything from a government takeover of your assets to higher tax rates or royalty demands out of the blue, to worker strikes and mine shutdowns, does happen in the less-stable areas of the world.

In my experience, an investor needs to triangulate the earnings and cash flow future, versus reserves in the ground and balance sheet setup, against regional risks and possible worker demands. In my research, the reward side of the equation at $21 a share is now much smarter than asset-related risks. In this regard, AngloGold’s strong diversification of mine assets worldwide is definitely an advantage.

With proven reserves under 10 years, using last year’s outdated $1100 an ounce selling price assumption, an investor should demand a very high level of earnings against little debt. And this is the case for AngloGold with little debt vs. cash generation today (the company has been aggressively paying off debt with the 2019-20 bump higher in precious metals).

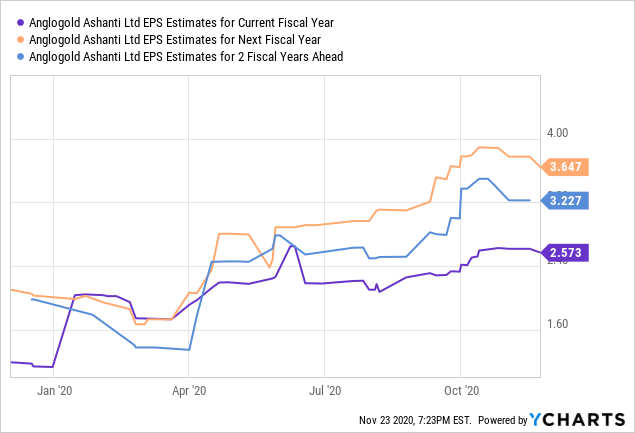

Free cash flow is estimated as high as $1 billion and after-tax earnings approaching $2 billion annually for 2021-22. These numbers compare quite favorably to a $9.4 billion equity market cap at $21 per share price. They are the lowest operating multiples of any of the major producers.

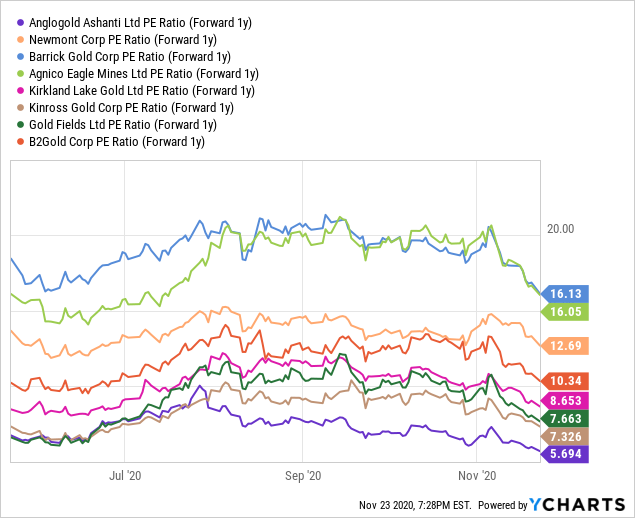

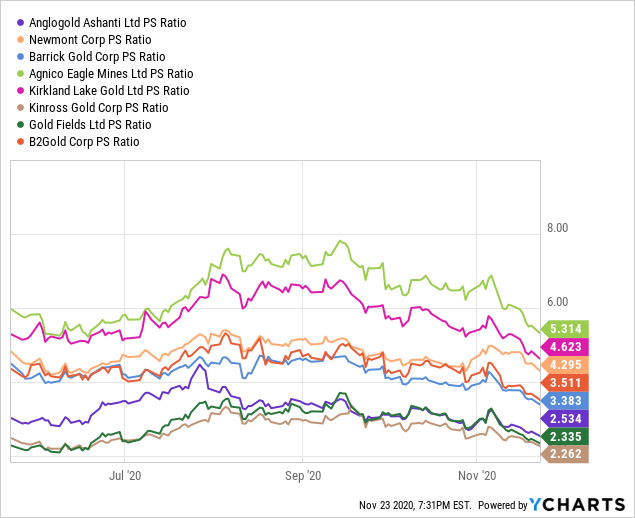

Low P/E Valuation

Below are some charts of projected income growth per share the next two years and AngloGold’s low 1-year forward, forecasted P/E ratio of 5.6x. Measured against the majors earning a profit today, the enterprise’s basic valuation multiple is eye-popping. The peer/competitor list includes Newmont Corp. (NEM), Barrick Gold Corp.(GOLD), Agnico Eagle Mines (AEM), Kirkland Lake Gold (KL), Kinross Gold Corp. (KGC), Gold Fields Limited (GFI) and B2Gold Corp. (BTG).

Price-to-trailing 12-month sales is also low for the group. This gives tremendous leverage to AngloGold shares, if a large gold/silver price upswing is in the cards for 2021.

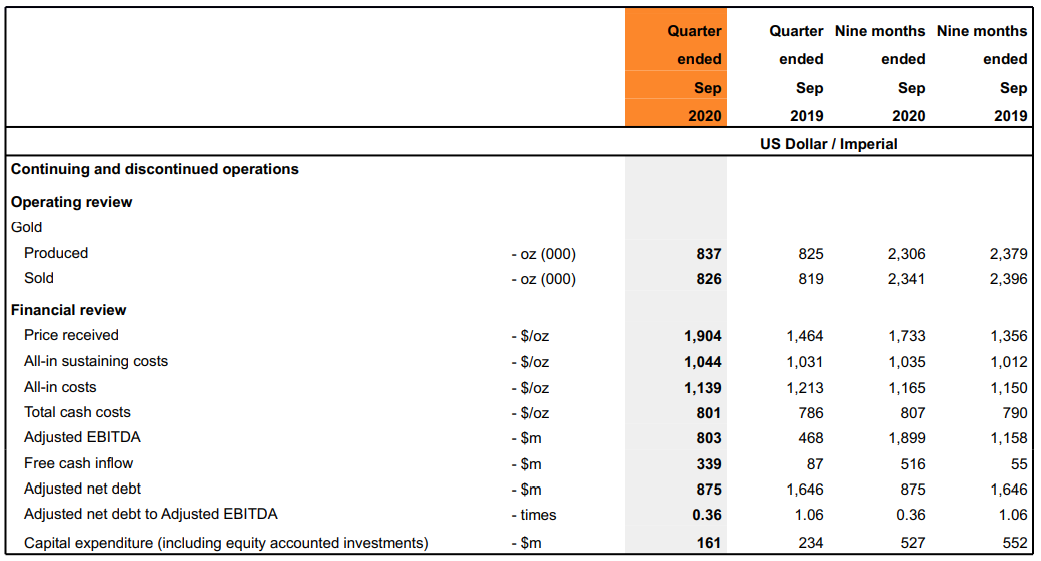

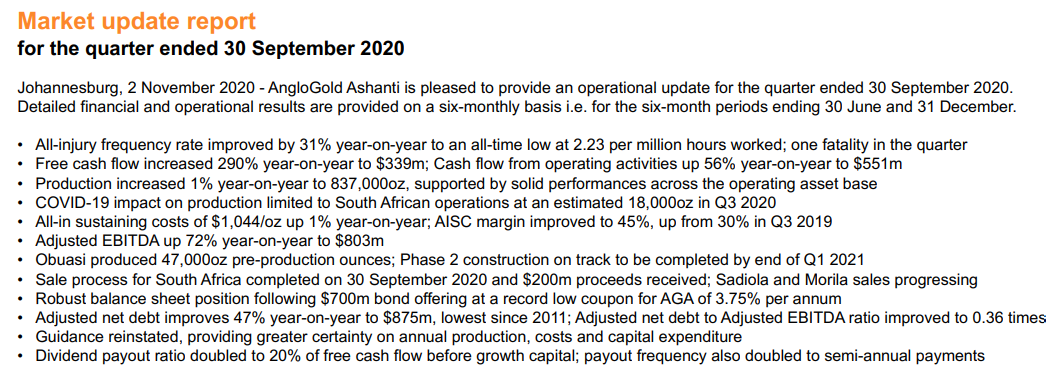

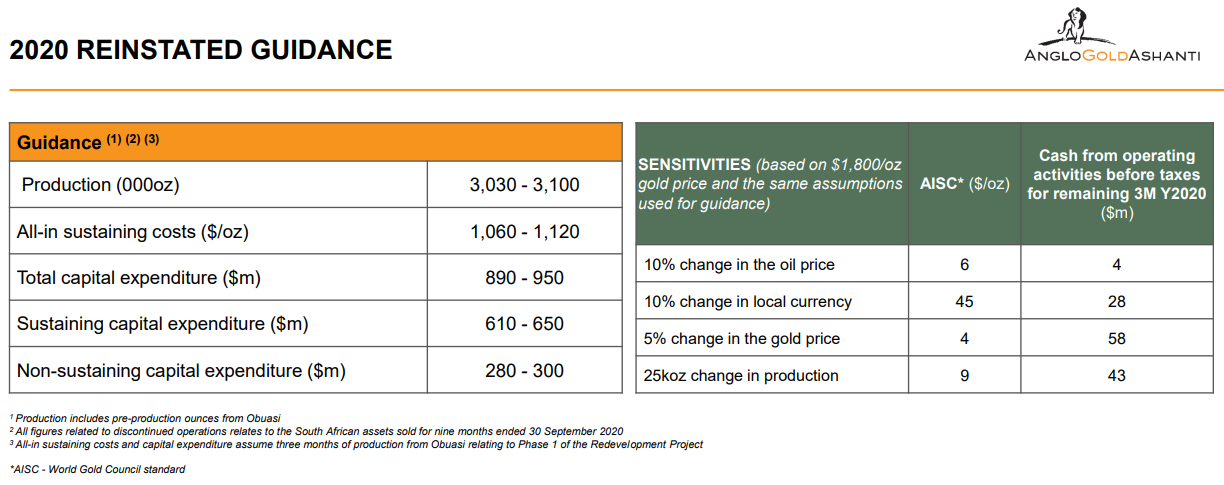

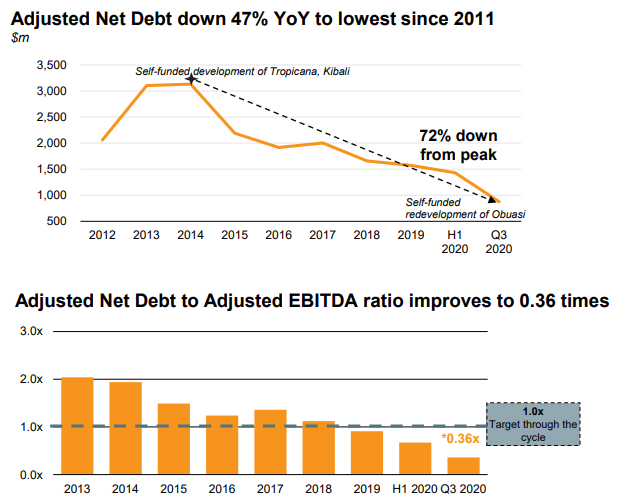

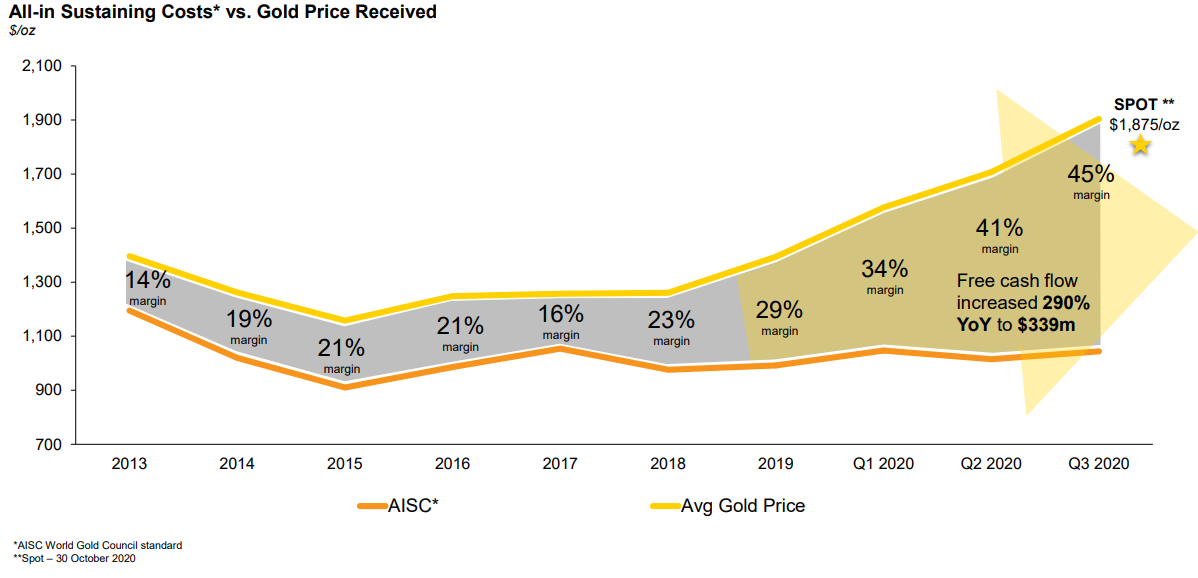

Cash flow and profit margins have improved dramatically the last several years, resulting from smart asset development and higher gold/silver prices. Below are some operating highlights from the September quarter just ended, with guidance projections by the company.

Image Source: Q3 Earnings Report

Some graphs reviewing the tremendous strides made during 2020 in paying down debt and expanding operating margins are shown below.

Image Source: Company Presentation

Technical Momentum

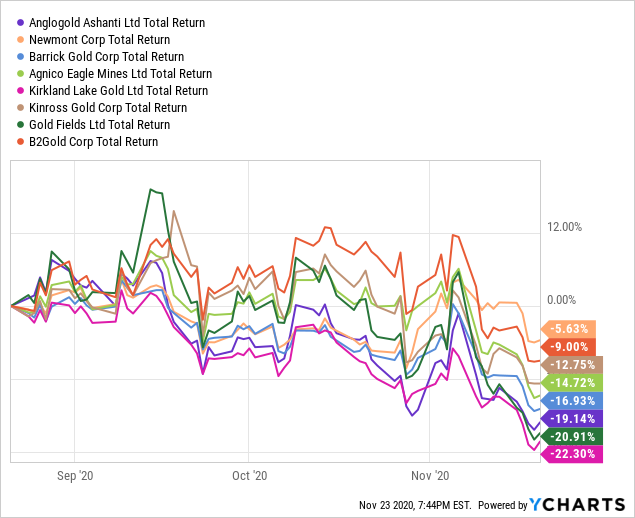

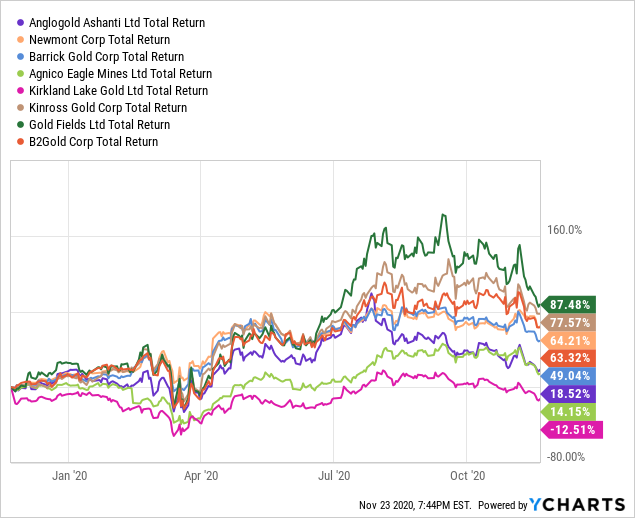

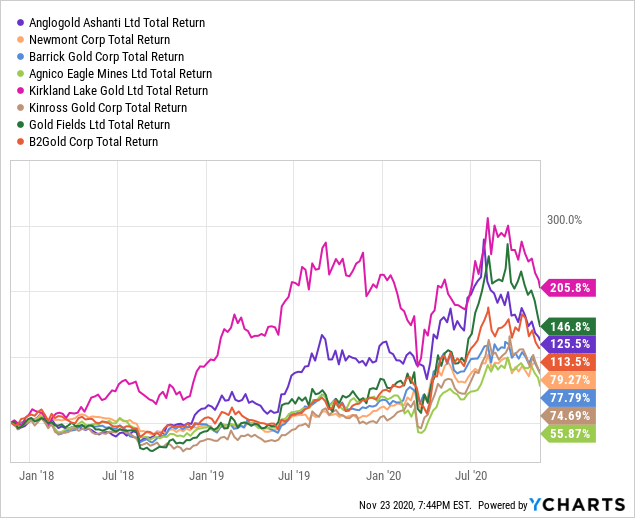

AngloGold stock was a leading industry performer for several years into the July peak quote. I have charted some total return graphs, including dividends, below from 3 months to 3 years in duration.

Notice, AngloGold was tied with Kirkland Lake Gold in July for the top spot on the trailing 3-year chart. The drop since summertime has reached an excessive level, in my opinion, and convinced me to open a position.

The rise in AngloGold has been supported by the strong uptrend in gold and silver prices. Low precious metals valuations relative to other assets existed three years ago.

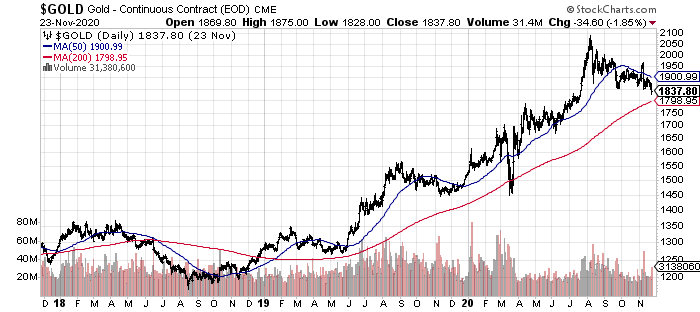

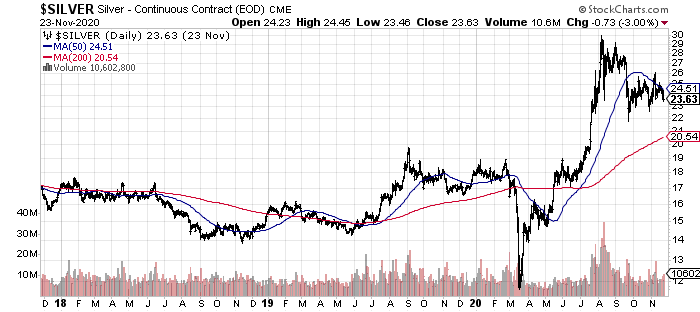

Then sprinkle on record central bank money printing globally to deal with the coronavirus economic mess, and the related paper currency devaluation trend has brought in plenty of investor interest to hard money plays like gold/silver miners. Spot gold and silver prices in U.S. dollars are drawn below, over a 3-year period.

For AngloGold shares, I have drawn a 2-year chart. Despite the sharp rise in metals pricing, new investment capital can purchase the company at the same level as 18 months ago! While the share price was likely ahead of itself in the middle of 2019, today’s quote and valuation is extremely compelling, especially if gold/silver are set to recover to new highs next year.

I have also listed some of my favorite momentum indicators on the chart. The Accumulation/Distribution Line, Negative Volume Index and On Balance Volume signals had been quite bullish in 2019. They turned into a mixed bag during 2020, mirroring stock price swings. The truly bullish note I would highlight is circled in red below.

The Negative Volume Index (NVI) has been in a slightly rising trend since August. During a large downturn in price, this often signals lots of buying interest on weakness. In fact, it records more buying than selling volume on slower trading days. The NVI movements are the most bullish in years relative to overall price change. It may be telegraphing a lack of share supply, if the gold and silver price can reverse the second-half pullback. A recovery into a solid precious metals upswing during 2021 may propel the quote back above $30 without much buying effort.

Final Thoughts

The strongest part of the seasonal pattern in gold and silver markets occurs between early December and February each year. I talked about this recurring bullish situation in an article posted November 2019 here. If history holds true and we see a nice rebound in the monetary precious metals into February 2021, AngloGold Ashanti could be a terrific buy right now.

I am modeling gains of 20-50% from $21 a share during the course of the next 6-12 months, assuming just a minor rise in gold/silver prices. If new highs are coming next year, with gold priced near $2500 an ounce and silver quoted around $30, AngloGold could double the present quote.

Smart management of free cash flow should reduce AngloGold’s net debt closer to zero the next 12-24 months, leaving plenty of extra cash for new acquisitions and mine development. Another bullish possibility to contemplate is the company’s low fundamental valuation could encourage a takeover attempt by one of the mentioned peers or a base metals miner.

I purchased shares of AngloGold recently in the context of a larger, diversified gold/silver portfolio of investments. I prefer and suggest you buy the simple gold/silver bullion ETFs first, such as the SPDR Gold Trust ETF (GLD) or the iShares Silver Trust ETF (SLV), weighting them as the greatest positions with your capital.

Safer, North American miners would be next, like Newmont. Then you can buy other miners down the risk scale, including AngloGold Ashanti, some mid-tier miners and exploration resource assets, to round out a portfolio design.

If you are new to gold/silver stocks, or just want a single diversified-mining hedge product for your portfolio, I am using the iShares MSCI Global Gold Miners ETF (RING) in my weightings. I wrote about the ETF’s prospects last week here. AngloGold is a part of RING.

Thanks for reading. This article should be a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Disclosure: This writing is for informational purposes only. All opinions expressed herein are not investment recommendations, and are not meant to be relied upon in investment decisions. The author is not acting in an investment advisor capacity and is not a registered investment advisor. The author recommends investors consult a qualified investment advisor before making any trade. This article is not an investment research report, but an opinion written at a point in time. The author’s opinions expressed herein address only a small cross-section of data related to an investment in securities mentioned. Any analysis presented is based on incomplete information, and is limited in scope and accuracy. The information and data in this article are obtained from sources believed to be reliable, but their accuracy and completeness are not guaranteed. Any and all opinions, estimates, and conclusions are based on the author’s best judgment at the time of publication, and are subject to change without notice. Past performance is no guarantee of future returns.

{kind=link}