Global economy approaches soft landing, but risks remain

The clouds are beginning to part. The global economy begins the final descent toward a soft landing, with inflation declining steadily and growth holding up. But the pace of expansion remains slow, and turbulence may lie ahead.

Global activity proved resilient in the second half of last year, as demand and supply factors supported major economies. On the demand side, stronger private and government spending sustained activity, despite tight monetary conditions. On the supply side, increased labor force participation, mended supply chains and cheaper energy and commodity prices helped, despite renewed geopolitical uncertainties.

This resilience will carry over. Global growth under our baseline forecast will steady at 3.1 percent this year, a 0.2 percentage point upgrade from our October projections, before edging up to 3.2 percent next year.

Important divergences remain. We expect slower growth in the United States, where tight monetary policy is still working through the economy, and in China, where weaker consumption and investment continue to weigh on activity. In the euro area, meanwhile, activity is expected to rebound slightly after a challenging 2023, when high energy prices and tight monetary policy restricted demand. Many other economies continue to show great resilience, with growth accelerating in Brazil, India, and Southeast Asia’s major economies.

Inflation continues to ease. Excluding Argentina, global headline inflation will decline to 4.9 percent this year, down 0.4 percentage point from our October projection (also excluding Argentina). Core inflation, excluding volatile food and energy prices, is also trending lower. For advanced economies, headline and core inflation will average around 2.6 percent this year, close to central banks’ inflation targets.

With the improved outlook, risks have moderated and are balanced. On the upside:

- Disinflation could happen faster than anticipated, especially if labor market tightness eases further and short-term inflation expectations continue to decline, allowing central banks to ease sooner.

- Fiscal consolidation measures that governments have announced for 2024-25 may be delayed as many countries face rising calls for increased public spending in what is the biggest global election year in history. This could boost economic activity, but also spur inflation and increase the prospect of disruption later.

- Looking further ahead, rapid improvement in Artificial Intelligence could boost investment and spur rapid productivity growth, albeit one with significant challenges for workers.

On the downside:

- New commodity and supply disruptions could occur, following renewed geopolitical tensions, especially in the Middle East. Shipping costs between Asia and Europe have increased markedly, as Red Sea attacks reroute cargoes around Africa. While disruptions remain limited so far, the situation remains volatile.

- Core inflation could prove more persistent. The price of goods remains historically elevated relative to that of services. The adjustment could take the form of more persistent services—and overall—inflation. Wage developments, particularly in the euro area, where negotiated wages are still on the rise, could add to price pressures.

- Markets appear excessively optimistic about the prospects for early rate cuts. Should investors re-assess their view, long-term interest rates would increase, putting renewed pressure on governments to implement more rapid fiscal consolidation that could weigh on economic growth.

Policy challenges

With inflation receding and growth remaining steady, it is now time to take stock and look ahead. Our analysis shows that a substantial share of recent disinflation occurred via a decline in commodity and energy prices, rather than through a contraction of economic activity.

Since monetary tightening typically works by depressing economic activity, a relevant question is what role, if any, has monetary policy played? The answer is that it worked through two additional channels. First, the rapid pace of tightening helped convince people and companies that high inflation would not be allowed to take hold. This prevented inflation expectations from persistently rising, helped dampen wage growth, and reduced the risk of a wage-price spiral. Second, the unusually synchronized nature of the tightening lowered world energy demand, directly reducing headline inflation.

But uncertainties remain and central banks now face two-sided risks. They must avoid premature easing that would undo many hard-earned credibility gains and lead to a rebound in inflation. But signs of strain are growing in interest rate-sensitive sectors, such as construction, and loan activity has declined markedly. It will be equally important to pivot toward monetary normalization in time, as several emerging markets where inflation is well on the way down have started doing so already. Not doing so would jeopardize growth and risk inflation falling below target.

My sense is that the United States, where inflation appears more demand-driven, needs to focus on risks in the first category, while the euro area, where the surge in energy prices has played a disproportionate role, needs to manage more the second risk. In both cases, staying on the path toward a soft landing may not be easy.

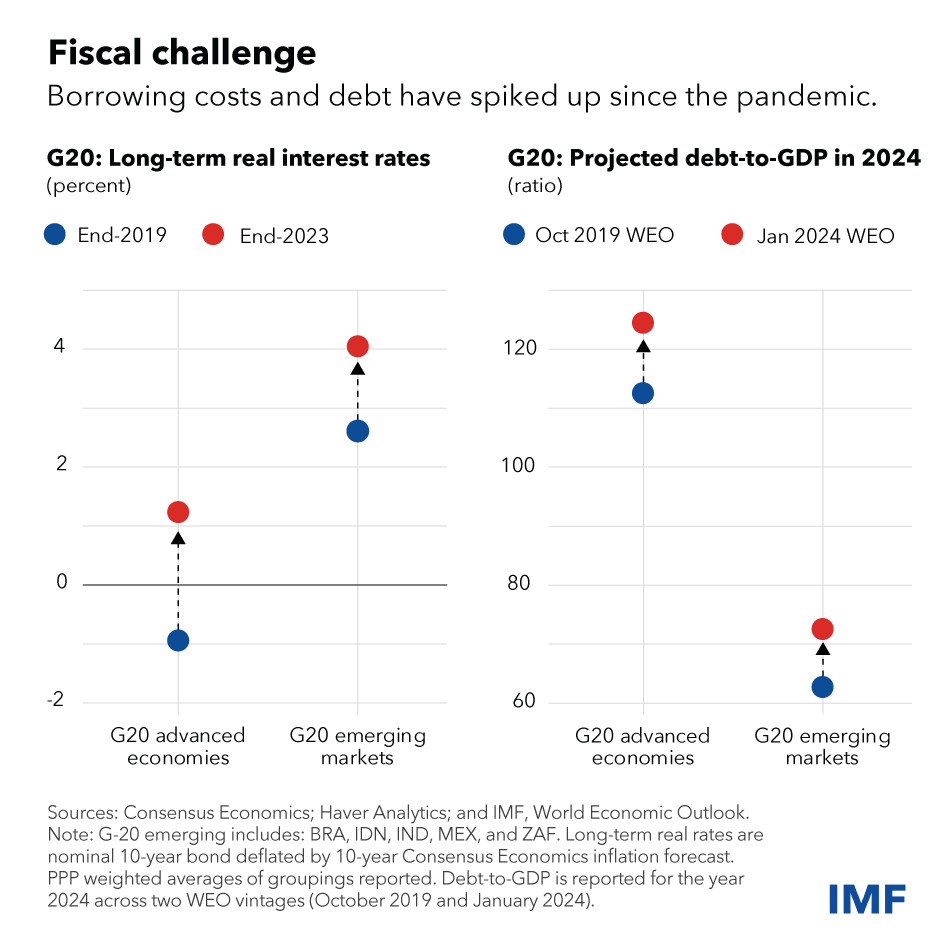

The biggest challenge ahead of us is to tackle elevated fiscal risks. Most countries came out of the pandemic and energy crisis with higher public debt levels and borrowing costs. Bringing down public debt and deficits will give space to deal with future shocks.

Remaining fiscal measures introduced to offset high energy prices should be phased out right away, as the energy crisis is behind us. But more is needed. The danger is two-fold. The most pressing risk is that countries do too little. Fiscal fragilities will build up until the risk of a fiscal crisis forces sudden and disruptive adjustments, at great cost. The other risk, already relevant for some countries, is to do too much, too soon, in the hope of convincing markets of ones’ fiscal rectitude. This could endanger growth prospects. It would also make it much harder to address imminent fiscal challenges such as the climate transition.

What to do then? The answer is to implement a steady fiscal consolidation, with a non-trivial first installment. Promises of future adjustment alone will not do. This first installment should be combined with an improved and well-enforced fiscal framework, so future consolidation efforts are both sizable and credible. As monetary policy starts to ease and growth resumes, it should become easier to do more. The opportunity should not be wasted.

Emerging markets have been very resilient, with stronger-than-expected growth and stable external balances, partly due to improved monetary and fiscal frameworks. Yet divergence in policy between countries may spur capital outflows and currency volatility. This calls for stronger buffers, in line with our Integrated Policy Framework.

Beyond fiscal consolidation, the focus should return to medium-term growth. We project global growth of 3.2 percent next year, still well below the historical average. A faster pace is needed to address the world’s many structural challenges: the climate transition, sustainable development, and raising living standards.

Reforms that ease the most binding constraints to economic activity, such as governance, business regulation and external sector reform, can help unleash latent productivity gains, our research shows. Stronger growth could also come from limiting geoeconomic fragmentation by, for instance, removing the trade barriers that are impeding trade flows between different geopolitical blocs, including in low-carbon technology products that are crucially needed by emerging and developing countries.

Instead, we should strive to keep our economies more interconnected. Only by doing so can we work together on shared priorities. Multilateral cooperation remains the best approach to address global challenges. Progress toward that, such as the recent 50 percent increase of the Fund’s permanent resources, is welcome.

{kind=link}