- IMF says global imbalances are widening again, and tariffs will not fix them

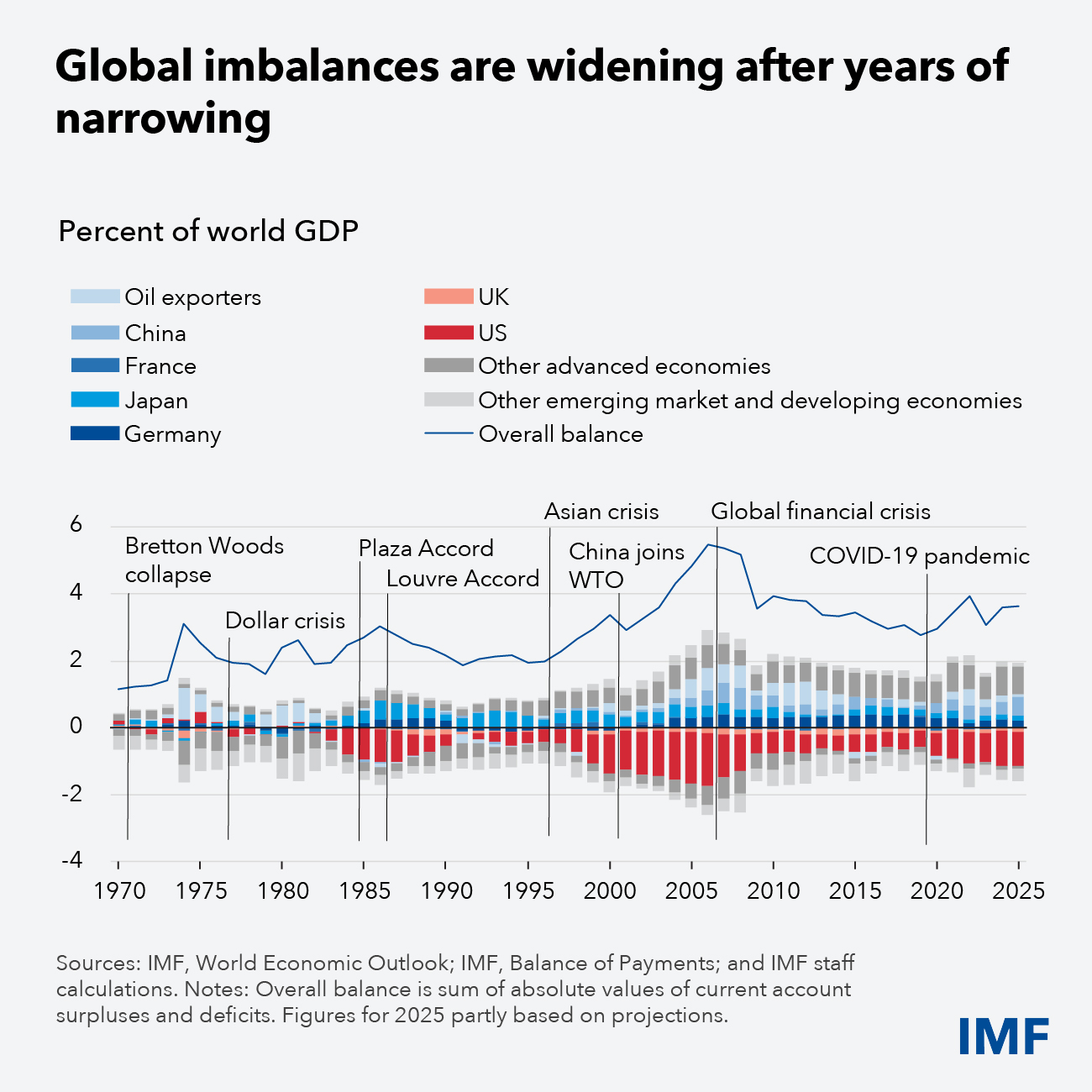

The International Monetary Fund has warned that global imbalances are widening again and has pushed back against the idea that tariffs or narrow industrial interventions can meaningfully resolve them, arguing instead that the deeper drivers are rooted in domestic saving, investment, and macroeconomic policy choices.

In a policy discussion at the start of April, the IMF Executive Board supported a staff paper on global imbalances that comes at a sensitive time for the world economy: trade tensions are rising, current account surpluses and deficits remain concentrated and persistent, and policymakers are increasingly using industrial policy and trade restrictions as tools of economic statecraft.

The Fund’s message is uncomfortable for many governments because it redirects attention away from the politics of blaming trading partners and back towards the harder issue of domestic adjustment. Its central analytical claim is that the balance between national saving and investment still shapes current account positions. In that framework, countries do not eliminate external imbalances simply by taxing imports or by promoting favoured sectors. They do so by changing the underlying policy mix that drives spending, savings behaviour, fiscal balances, and domestic demand.

That is why the IMF’s findings are more radical than they first appear. In a world where trade policy has become a front-line political instrument, the Fund is effectively saying that much of the current debate is aimed at the symptom rather than the cause.

The paper finds that traditional macroeconomic policies remain the dominant force behind global imbalances. By contrast, sector-specific or “micro” industrial policies generally have limited and ambiguous effects on current account positions, depending on whether they raise productivity enough to alter broader saving and investment decisions. Even tariffs, often presented as a direct corrective tool, are unlikely to have much lasting effect on external balances unless used only temporarily or linked to policies that increase public saving.

That conclusion matters because it cuts through a growing assumption in global policymaking: that economic nationalism can substitute for macroeconomic discipline. The IMF’s answer is that it cannot do this without cost.

The Fund does leave room for a more consequential role for economy-wide or “macro” industrial policies, especially when paired with measures such as capital flow restrictions or sustained reserve accumulation. But even here, the tone is cautionary. Such strategies may have a more material impact on external balances, yet they often do so by suppressing domestic consumption and creating spillovers for other countries. In other words, they may work arithmetically while weakening welfare. The more thought-provoking part of the IMF’s argument lies in what it says about adjustment. The Fund’s scenario analysis suggests that the best outcome does not come from one country adjusting alone or from deficit countries absorbing all the pain. Instead, it comes from simultaneous domestic rebalancing in both surplus and deficit economies. If undertaken together, this process can reduce global imbalances while also lifting overall world output.

This is an important point because it reframes rebalancing as a collective action problem. Persistent imbalances are not merely technical outcomes in trade data; they reflect asymmetric policy choices across major economies. And if those choices are not corrected together, the adjustment burden tends to fall unevenly, often resulting in financial instability, abrupt capital flow shifts, or politically explosive trade confrontations.

The Executive Board broadly endorsed that view. Directors said large and persistent surpluses or deficits that go beyond what fundamentals justify should be closely assessed because of the risks they pose to macroeconomic and financial stability. They also reaffirmed that trade and industrial policies cannot substitute for reforms that support productivity, resilient domestic demand and macroeconomic stability.

For emerging and frontier economies, including those in Africa, the implications are significant. Global imbalances are often discussed as if they are problems belonging only to the world’s largest economies. In reality, smaller economies live with their spillovers. When major countries fail to rebalance in an orderly way, the consequences are felt through volatile capital flows, exchange-rate pressure, commodity swings and tighter external financing conditions. That is an inference from the Fund’s emphasis on spillovers, stock-flow dynamics and financial stability risks.

For Ghana, this matters in a direct way. A small open economy trying to stabilise after debt distress is especially exposed to the disorderly side of global adjustment. If major deficit economies continue to rely on debt-financed demand, while major surplus economies continue to suppress consumption or lean on reserve accumulation, the resulting distortions can keep the global financial system unstable in ways that raise borrowing costs and narrow policy space for countries with far less room to absorb shocks.

The IMF is therefore making a broader plea for even-handed surveillance and international cooperation at a time when both are becoming harder to sustain. Directors called for better data, refinement of the External Balance Assessment models and more transparent analysis of trade and industrial policies. They also stressed that monitoring imbalances must extend beyond current account flows to include capital movements, external balance sheets and stock positions.

That emphasis on stock positions is especially important. Countries can run imbalances for years without immediate crisis, but the longer they do so, the more vulnerable the system becomes to shifts in investor expectations, valuation effects and abrupt reversals. This is where what looks manageable in flow terms can suddenly become destabilising in financial terms. The Fund’s conclusion is ultimately a rebuke to easy policy theatre. Durable rebalancing, it argues, will not come from symbolic tariff hikes or fashionable industrial policy slogans. It will come from politically difficult domestic reforms undertaken across major economies at the same time.

{kind=link}