Why we must resist geoeconomic fragmentation—and how

As policymakers and business leaders head to Davos, the global economy faces perhaps its biggest test since the Second World War.

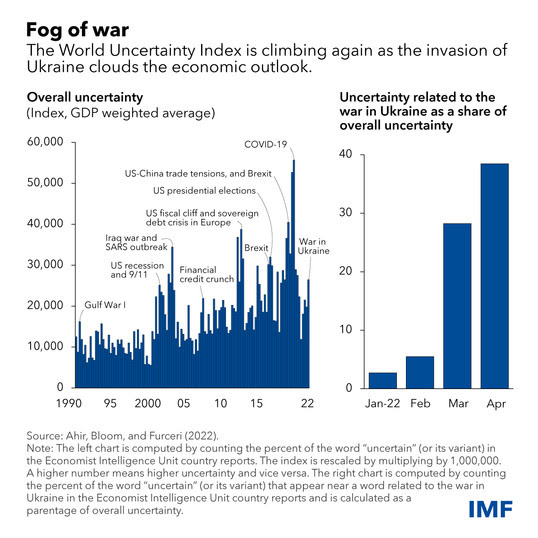

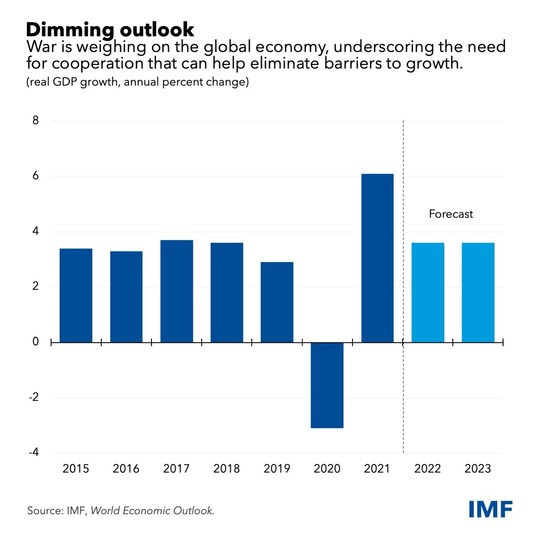

Russia’s invasion of Ukraine has compounded the Covid-19 pandemic—a crisis upon a crisis—devastating lives, dragging down growth, and pushing up inflation. High food and energy prices are weighing heavily on households around the world. Tightening financial conditions are putting further pressure on highly indebted nations, companies, and families. And countries and companies are re-evaluating global supply chains amid persistent disruptions.

Add to this sharply increased volatility in financial markets and the continuing threat of climate change, and we face a potential confluence of calamities.

Yet our ability to respond is hampered by another consequence of the war in Ukraine—the sharply increased risk of geoeconomic fragmentation.

How did we get here? Over the past three decades, flows of capital, goods, services, and people have transformed our world, helped by the spread of new technologies and ideas. These forces of integration have boosted productivity and living standards, tripling the size of the global economy and lifting 1.3 billion people out of extreme poverty.

But the successes of integration have also brought complacency. Inequalities of income, wealth, and opportunity have continued to worsen within too many countries for a long time—and across countries in recent years. People have been left behind as industries have changed amid global competition. And governments have struggled to help them.

Tensions over trade, technology standards, and security have been growing for many years, undermining growth—and trust in the current global economic system. Uncertainty around trade policies alone reduced global gross domestic product in 2019 by nearly 1 percent, according to IMF research. And since the war in Ukraine started, our monitoring indicates that around 30 countries have restricted trade in food, energy, and other key commodities.

The costs of further disintegration would be enormous across countries. And people at every income level would be hurt—from highly-paid professionals and middle-income factory workers who export, to low-paid workers who depend on food imports to survive. More people will embark on perilous journeys to seek opportunity elsewhere.

Think of the impacts of reconfigured supply chains and higher barriers to investment. They could make it more difficult for developing nations to sell to the rich world, gain know-how, and build wealth. Advanced economies would also have to pay more for the same products, stoking inflation. And productivity would suffer as they lost partners who currently co-innovate with them. IMF research estimates technological fragmentation alone can lead to losses of 5 percent of GDP for many countries.

Or think of the new transaction costs on people and businesses if countries develop parallel, disconnected payment systems to mitigate the risk of potential economic sanctions.

So, we have a choice: Surrender to the forces of geoeconomic fragmentation that will make our world poorer and more dangerous. Or reshape how we cooperate—to make progress on addressing collective challenges.

Restoring Trust in the Global System—Four Priorities

To restore trust that the rules-based global system can work well for all countries, we must weave our economic fabric in new and better ways. If we can start by focusing on urgent issues where progress will clearly benefit everyone, we can build the trust needed to cooperate in other areas where there is disagreement.

Here are four priorities that can only be advanced by working together.

First, strengthen trade to increase resilience.

We can start now by lowering trade barriers to alleviate shortages and lower the prices of food and other products.

Not only countries but also companies need to diversify imports—to secure supply chains and preserve the tremendous benefits to business of global integration. While geostrategic considerations will drive some sourcing decisions, this need not lead to disintegration. Business leaders have an important role to play in this regard.

New IMF research shows that diversification can cut potential GDP losses from supply disruptions in half. Auto manufacturers and others have found that designing products that can use substitutable or more widely available parts can reduce losses by 80 percent.

Diversifying exports can also increase economic resilience. Policies that help include: enhancing infrastructure to help businesses shorten supply chains, increasing broadband access, and improving the business environment. The WTO can also help with its overall support for more predictable, transparent trade policies.

Second, step up joint efforts to deal with debt.

With roughly 60 percent of low-income countries with significant debt vulnerabilities, some will need debt restructuring. Without decisive cooperation to ease their burdens, both they and their creditors will be worse off. But a return to debt sustainability will draw new investment and spur inclusive growth.

That is why the Group of Twenty’s Common Framework for Debt Treatment must be improved without delay. This means putting in place clear procedures and timelines for debtors and creditors—and making the framework available to other highly-indebted vulnerable countries.

Third, modernize cross-border payments .

Inefficient payment systems are another barrier to inclusive growth. Take remittances: the average cost of an international transfer is 6.3 percent. This means some $45 billion per year are diverted into the hands of intermediaries—and away from millions of lower-income households.

A possible solution? Countries could work together to develop a global public digital platform—a new piece of payment infrastructure with clear rules—so that everyone can send money at minimal cost and maximum speed and safety. It could also connect various forms of money, including central bank digital currencies.

Fourth, confront climate change: the existential challenge that looms above everything .

During the COP26 climate conference, 130 countries, representing over 80 percent of global emissions, committed to achieve net-zero carbon by around mid-century.

But we urgently need to close the gap between ambition and policy. To accelerate the green transition, the IMF has argued for a comprehensive approach that combines carbon pricing and investment in renewables, and compensation for those adversely affected.

Progress for People

The hard fact is that we have all been too slow to act as our economic fabric started to fray. But if countries can find ways now to come together around these urgent issues that transcend national borders and impact us all, we can begin to mitigate fragmentation and bolster cooperation. There are some hopeful signs.

When the pandemic hit, governments took coordinated monetary and fiscal measures to prevent another Great Depression. International cooperation was essential to developing vaccines in record time. On global corporate taxation, 137 countries agreed on reforms to ensure that multinational enterprises pay their fair share wherever they operate.

Last year, the IMF’s membership supported a historic $650 billion allocation of the Fund’s Special Drawing Rights to strengthen countries’ reserves. Even more recently, our members agreed to create the Resilience and Sustainability Trust—which provides longer-term affordable financing to help our more vulnerable members address climate change and future pandemics.

In the pursuit of further progress, we must all adhere to a simple guiding principle: policies are for people. Instead of globalizing profits, we should act to localize the benefits of a connected world.

Start with the communities in every country that lost out in the “old globalization,” and were set back further by the pandemic: Invest in their health and education. Help displaced workers learn in-demand skills and transition to careers in expanding industries. For example, firms that export pay higher salaries on average—as do greener jobs.

Multilateral institutions can also play a key role in reshaping global cooperation and resisting fragmentation, including by further strengthening their governance to ensure they reflect changing global economic dynamics—the upcoming IMF review of capital and voting shares will provide such an opportunity.

They can also leverage their convening power, and maximize use of their diversified toolkits. The IMF can help, for example, with its range of financial instruments, bilateral and global surveillance, and even-handed approach across our membership.

There is no silver bullet to address the most destructive forms of fragmentation. But by working with all stakeholders on urgent common concerns, we can begin to weave a stronger, more inclusive global economy.

{kind=link}