Argentina, Turkey lure investors seeking high-yield bond returns

Global investors are ramping up bets in some of the world’s riskiest bonds, convinced the debt will extend its spectacular rally as the threat of default subsides in emerging markets.

High-yielding government bonds — from Argentina to Turkey and Zambia — are once again luring money managers as policymakers promise reform, restructuring deals materialize and default risks abate. The strategy handed investors in emerging-market junk bonds 18.5% last year, nearly triple the returns in investment-grade sovereign debt, according to data compiled by Bloomberg.

“We have overweights across the high-yield space in a select group of countries — and we believe in those fiscal consolidation stories,” said David Robbins, an investor who oversees the $3.7 billion emerging-market debt fund at TCW. Plus, “you probably won’t see any defaults in the sovereign space.”

TCW is among those on Wall Street — including Neuberger Berman Group, M&G Investments and PGIM Fixed Income — that see momentum forming behind riskier developing-market debt in 2024. Speculation that the Federal Reserve will start reducing interest rates this year stands to make borrowing more affordable for lower-rated bondsellers. And a potential soft landing in the global economy is seen boosting appetite for risky assets.

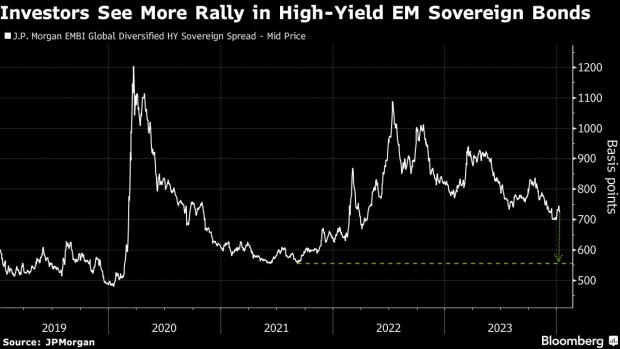

The extra yield investors demand to hold junk bonds from emerging-market governments over US Treasuries still lingers well above the mid-2021 level. To Neuberger’s co-head of the emerging markets debt team, Gorky Urquieta, there’s still “significant pick up” in the sovereign high-yield universe.

Investing in lower-rated debt comes with an expected dose of uncertainty. As traders question the outlook for central bank pivots, a gauge of sovereign emerging-market bonds — which includes both high-grade and low-grade notes — has dropped about 1.6% so far this year, according to data compiled by Bloomberg as of Jan. 11.

Low-rated bondsellers have also been largely left out of January’s deluge of new bond sales. But as long as major policymakers choose to pivot, the market is likely to reopen for riskier borrowers, according to Morgan Stanley strategist Simon Waever. Angola, Nigeria, Kenya and El Salvador are prime contenders to tap international bond markets this year at yields around 10%, he wrote in a note to clients.

“With lower US Treasury yields, many high-yield issuers are likely to regain market access over the next 12 months,” according to Carlos de Sousa and Daniel Karnaus, portfolio managers at Vontobel Asset Management AG. That would help create “a virtuous cycle as the fear of default is taken off the table.”

Turnaround Stories

In certain low-rated bonds, the potential for upside goes beyond the global environment for interest rates, inflation and growth. Investors are closely watching the new administration of Javier Milei in Argentina, who has promised to free the sputtering economy from the pain of inflation above 211%.

So far this month, the South American country managed to deliver $1.5 billion in interest payments to bondholders and strike a deal with the International Monetary Fund that unlocks about $4.7 billion in funding.

“The balance of risk is still positive in that country,” said Eamon Aghdasi, an analyst for emerging-market country debt at Grantham Mayo Van Otterloo & Co. “You could, if things work out, see a continued nice performance in Argentina. We’re still overweight.”

Bonds from Argentina rose in the past week on positive news of bond payment and the IMF deal. The extra yield investors demand to hold the country’s debt, on average, has slid to 19 percentage points over US Treasuries from as much as 27 percentage points in October, according to JPMorgan Chase & Co. data.

For Emanuele Del Monte, portfolio manager of emerging-market fixed income at Eurizon Asset Management, Milei’s economic and fiscal promises could represent a turning point for the serial defaulter.

“There will be pushback from a certain segment of the society, and politically it’s gonna be very harsh to bring it along,” he said. “The plan is very ambitious and there could there be potential for this turnaround.”

In Turkey, meanwhile, President Recep Erdogan has laid out a path to orthodox policy making, appointing former Wall Street bankers to government posts. And the central bank has started to increase interest rates, a move that led Claudia Calich, the head of emerging-market debt at M&G Investments in London, to add exposure to Turkey’s local debt market.

The nation’s dollar debt handed investors gains of 18% last year, and the extra yield investors demand for the bonds has plunged since Erdogan’s reelection, according to a JPMorgan data. On Friday, Moody’s Investors Service lifted the outlook on the country’s credit rating to positive, citing decisive changes in policy.

“After the election last year, they’ve done a few changes in terms of economic policy, particularly with the central bank,” Calich said. “That has brought quite a bit of new credibility.”

TCW’s Robbins pointed to sovereign bonds across Sub-Saharan Africa, including Angola, Nigeria and Kenya. In Kenya, the finance ministry has vowed to make the final interest payment and principal on its $2 billion euro bond, sidestepping a potential default on the terms of the debt, which matures in June.

Debt negotiations underway in already-defaulted countries like Zambia and Ghana could also unlock opportunity, said Cathy Hepworth, head of emerging-market debt at PGIM Fixed Income. Debt from both nations have attractive recovery values depending on how restructuring talks pan out, she added.

{kind=link}