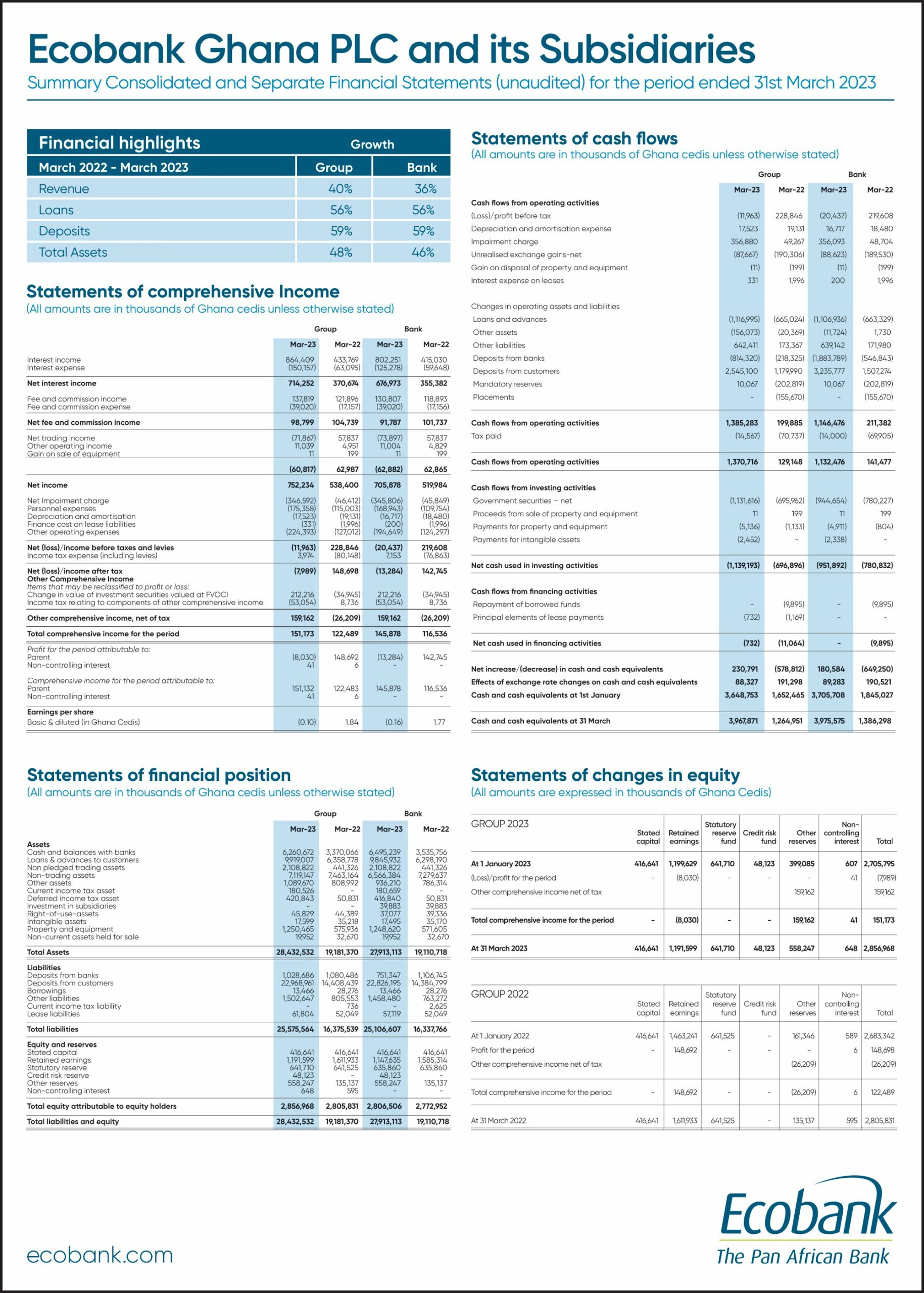

Assets of Ecobank Ghana rise to GHS 27.9bn in March 2023

Ecobank Ghana has announced a loss of GHS 13.2m for the period ending in March 2023 marking a significant decline from the GHS 142m profit posted in the same period the previous year (March 2023). The loss comes as a surprise and is likely to raise questions about the bank’s financial performance and strategic direction.

The loss has resulted in a sharp reduction in earnings per share, from GHS 1.77 to a loss of GHS 0.16, which is a cause for concern for investors and other stakeholders. The bank will need to take measures to address this decline and restore confidence in its financial performance.

Despite the loss, the bank has seen a rise in its assets from GHS 19.1bn to GHS 27.9bn, driven largely by increments in its cash and cash equivalents, loans and advances to customers, and non-pledged trading assets. This growth in assets indicates that the bank is expanding its operations and presence in the Ghanaian market, which could lead to improved financial performance in the future.

However, the bank’s liabilities have also grown significantly, from GHS 16.3bn to GHS 25.1bn within the review period, mainly driven by deposits from customers and banks. Deposits from customers accounted for GHS 22.8bn of the bank’s total liabilities at the end of 2022.

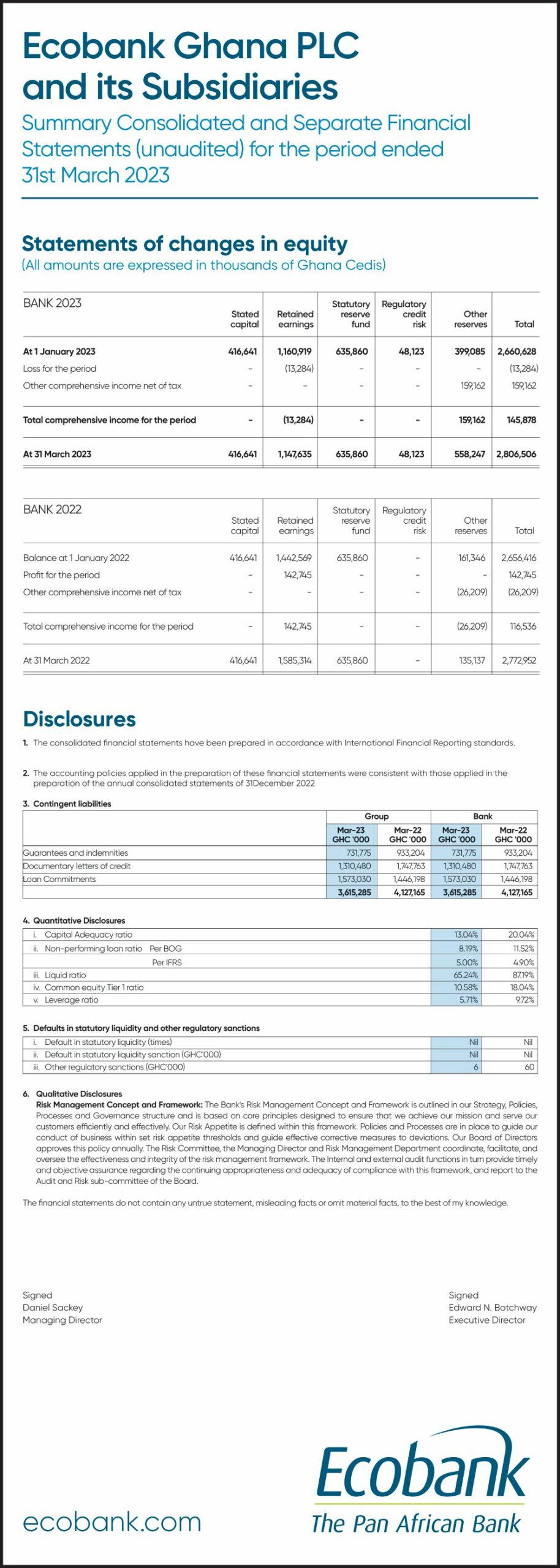

The bank’s Capital Adequacy Ratio has declined from 20% to 13% for the period under review, which is a cause for concern. A lower Capital Adequacy Ratio means that the bank has less of a cushion against unexpected losses, which could potentially impact its financial stability.

Despite the decline in the Capital Adequacy Ratio, the asset quality of the bank has improved as the non-performing loans declined from 11.52% to 8.19%. This improvement in asset quality indicates that the bank has been able to manage its credit risk effectively, which could lead to improved financial performance in the future.

The loss of GHS 13.2m is a significant setback for Ecobank Ghana, particularly considering the steep decline from the previous year’s profit. The bank’s growth in assets and reduction in non-performing loans are positive developments, but the decline in the Capital Adequacy Ratio is a cause for concern. The bank will need to take steps to improve its financial performance and strengthen its capital position in the coming years.

Ecobank Ghana’s financial performance for the period under review has been mixed, with a significant loss and a decline in the Capital Adequacy Ratio. However, the bank’s growth in assets and improvement in asset quality are positive developments that could lead to improved financial performance in the future. The bank will need to take measures to address its declining financial performance and restore confidence in its operations among investors and other stakeholders.

{kind=link}