Cal Bank reports decline in assets by GHS 800m due to decrease in investment securities, trading assets

Cal Bank, one of Ghana’s leading financial institutions, has reported a disappointing performance for the year 2022, as revealed in its recently released financial statements. The bank’s assets decreased from GHS 10bn at the end of December 2021 to GHS 9.2bn at the end of December 2022. This decline was largely attributed to a drop in the bank’s investment securities and non-pledged trading assets, which went down from GHS 4.9bn to GHS 2.6bn and GHS 672m to GHS 47m, respectively.

Furthermore, Cal Bank’s liabilities showed a minor decline of GHS 32m, from GHS 8.75bn in 2021 to GHS 8.72bn in 2022. This decrease could be seen as a silver lining amidst the otherwise bleak financial report.

However, the bank reported a net loss of GHS 815m at the end of 2022, which was attributed to the government’s domestic debt restructuring program. This is in stark contrast to the previous year, where Cal Bank recorded a profit of GHS 215m. Such a significant loss in profitability is a cause for concern, as it could undermine investor confidence in the bank and could hamper its ability to secure funding in the future.

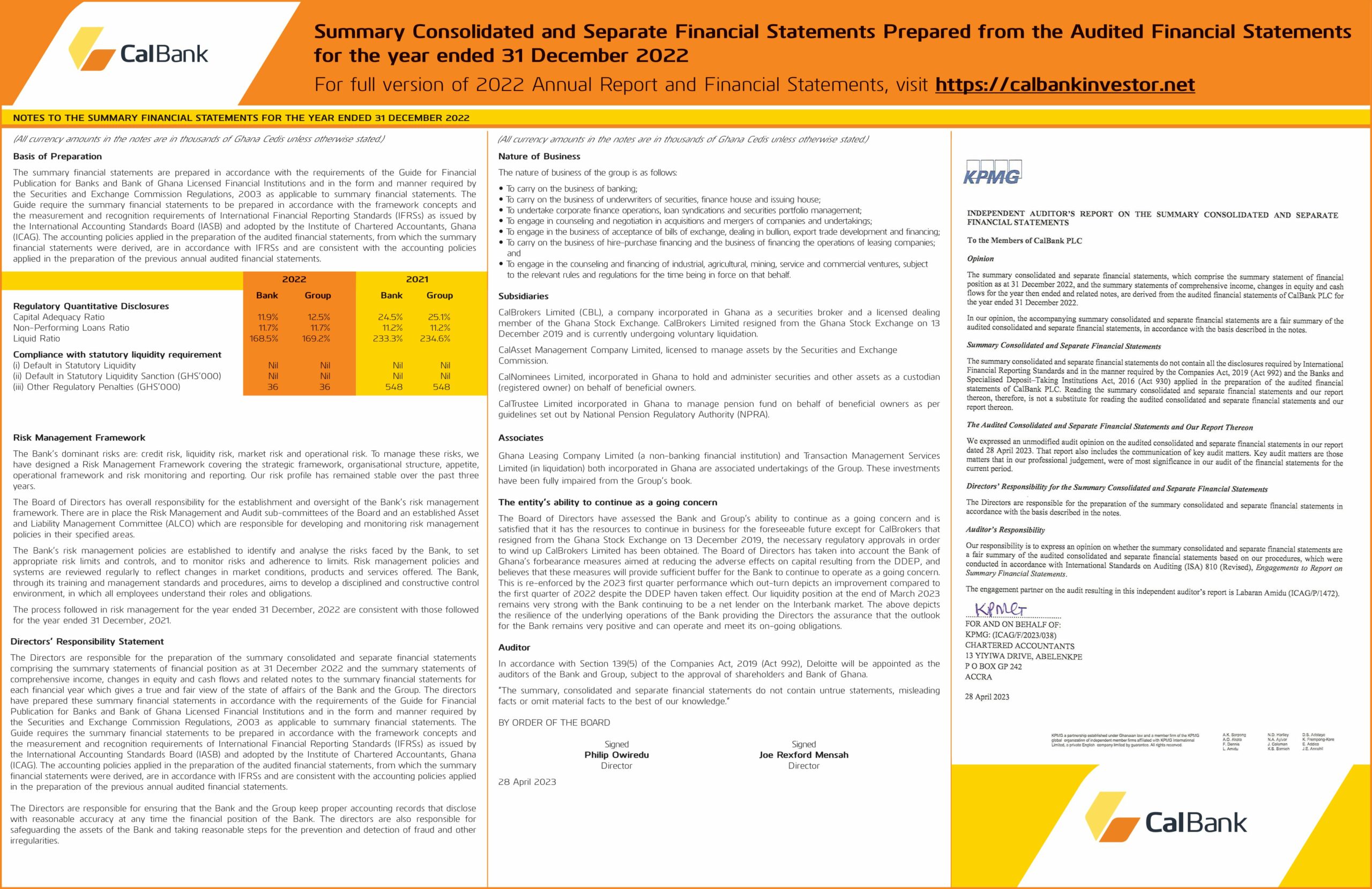

The capital adequacy ratio of the bank also saw a drastic drop from 24.5% in 2021 to 11.9% in 2022. Such a significant decline is not only worrying for the bank’s stakeholders but could also impact the bank’s lending capacity. This drop in the capital adequacy ratio could be attributed to the bank’s net loss in 2022, which has reduced the bank’s capital base.

Moreover, the bank’s asset quality showed a slight deterioration in 2022, with non-performing loans increasing from 11.2% at the end of 2021 to 11.7% at the end of 2022. This increase in non-performing loans could signal that the bank’s loan portfolio may have been affected by external factors such as the ongoing economic downturn in Ghana.

Cal Bank’s financial performance in 2022 has been a matter of concern, as its assets declined, its capital adequacy ratio dropped, and its non-performing loans increased. While the slight decline in liabilities could be seen as a silver lining, the bank’s net loss and its drop in profitability are significant issues that need to be addressed. The bank’s management will need to take proactive steps to address these challenges to improve its financial performance and reassure stakeholders.

{kind=link}