China’s hidden financial dangers erupt with shadow bank crisis

Only a week ago, Zhongzhi Enterprise Group Co. attracted little notice within China and was almost unheard of everywhere else.

Now, the secretive shadow banking giant has become the latest symbol of financial fragility in an $18 trillion economy where confidence among investors, businesses and consumers is rapidly dwindling.

The privately owned manager of more than 1 trillion yuan ($137 billion) and its trust-company affiliates are under intense scrutiny after halting payments to thousands of customers. To underline its importance, regulators have formed a task force as they seek to prevent contagion. Behind the scenes the firm has hired KPMG to carry out what is likely to be a protracted restructuring process. Potential asset sales threaten to hit broader markets.

Zhongzhi’s troubles have even sparked protests, prompting the police to intervene to order disgruntled clients not to go public in their desperation to recoup losses. As word of Zhongzhi’s difficulties spread, Chinese assets tumbled, helping pushing the yuan close to a 16-year low. A central bank rate cut this week has done little to bolster confidence as concerns about more failures in the nation’s $2.9 trillion trust sector mount.

“This is a problem that’s only going to intensify” with more funds missing payments, Kathy Lien, managing director of BK Asset Management said in an interview Thursday on BNN Bloomberg Television. “There is only so much they can do,” she said, referring to Beijing, calling this a “crisis of confidence.”

The failures represent another challenge for Beijing, already grappling with a weak economy, a property selloff and growing geopolitical tensions with the US.

For Zhongzhi, the pieces unraveled quickly, in the latest sign of hidden risk in China’s opaque financial sector. It all came to light with three stock exchange filings in Shanghai late last Friday, which sounded the alarm on missed payments on high-yield investment products offered by the firm and Zhongrong International Trust, a trust firm closely linked to Zhongzhi.

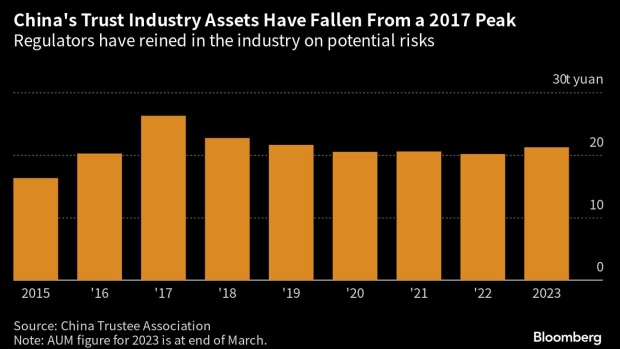

Zhongrong is a top-10 trust, pooling deposits from largely wealthy individual investors and companies to make investments in stocks, bonds and others assets, while lending to firms that can’t access traditional banks. Though they operate in the shadows, the trusts account for almost 10% of total loans in China, according to Bloomberg Economics.

Zhongrong has 270 products totaling 39.5 billion yuan due this year, according to data provider Use Trust.

To lure cash, trusts like Zhongrong offer rates as high as 6% or 8% for a one-year term, about double what commercial banks pay on similar products. With stocks in China tumbling and real estate in a two-year decline, these seemingly can’t-miss funds with quarterly payouts have attracted trillions of yuan.

The pitch worked for Joey, a client in northern China who invested about 2 million yuan — more than a quarter million dollars — into four Zhongrong products earning 4% to 6%. Several neighbors invested as well. She now wonders whether she will get any money back after payments stopped in June. Visits to the local regulator and police have been fruitless.

“We are very desperate,” Joey said, declining to give her full name because of privacy concerns. “We may have no choice but take to the streets sooner or later.”

Zhongzhi was founded as a lumber business in 1995 by Xie Zhikun, who before he passed away in 2021 made a fortune in printing before expanding into distressed assets including real estate.

Before Zhongzhi’s troubles emerged into the opening, it was already acting behind the scenes. In late July it hired KPMG to review its balance sheet amid a worsening liquidity crunch, people familiar said earlier, asking not to be identified as the matter is private. The Beijing-based company plans to restructure debt and sell assets after the review in order to repay investors, the people said.

It’s unclear how many products Zhongzhi has defaulted on and whether the company has sufficient assets to cover the shortfall if liquidated.

In recent years, even as rival trusts pared risks, Zhongzhi and its affiliates, especially Zhongrong, extended financing to troubled developers and snapped up assets from companies including China Evergrande Group.

The real estate investments soured after a crackdown on property lending and a slump in sales during the pandemic led to a flurry of defaults. Even developers like Country Garden Holdings Co. that survived the first wave of failures are under pressure as the slowdown continues. China’s home sales tumbled the most in a year last month, and Country Garden is on the verge of default after it missed coupon payments.

The property woes created a cash crunch for trusts like Zhongrong, which count on investments and loans to pay depositors. An estimated 10% of all trust assets — some $300 billion — are tied to the property sector, according to Bloomberg Economics.

Trouble in the trust sector is nothing new, but the size of Zhongzhi has ratcheted up concerns. About 106 trust products worth 44 billion yuan defaulted this year through July 31, according to Use Trust. Real estate investments accounted for 74% of the defaults by value. Last year also saw billions of dollars in defaults.

“The defaults could continue to hurt investor and market sentiment,” Fitch CreditSights analysts Zerlina Zeng and Karen Wu said in a note. “Disorderly winding-up of any large trust or wealth management company could test near-term financial stability.”

As payment delays mounted this week so did the protests.

About two dozen people rallied outside the firm’s Beijing offices, in a rare show of public outrage in the capital. In one of the video clips posted on Wechat seen by Bloomberg News, a woman is heard shouting: “Give us the money back, or we will die here.”

In an effort to quell the social unrest, China police responded swiftly, setting up metal gates around the office. They also visited the homes of several protesters, urging them to avoid public demonstrations, according to investors who asked not to be identified. The police visits spanned a massive area, including the southwestern province of Sichuan, and the coastal areas of Jiangsu and Shandong.

The failures have drawn attention from Beijing. The National Financial Regulatory Administration, China’s top banking regulator, established a working group to examine the risks at the financial holding company, according to people familiar. The regulator required Zhongrong to report its plans for future payments and assets that can be sold to deal with the liquidity crunch, said the people.

While it’s unlikely Zhongzhi’s woes will impact the big commercial banks, it could spread to other asset managers if wealthy investors start pulling their money, said Dinny McMahon, an analyst for Trivium China and author of China’s Great Wall of Debt.

“When investors start to lose faith, then all of a sudden an outfit’s ability to continue to raise new funds becomes more difficult,” McMahon said. “Then the potential for defaults to cascade becomes more and more.”

{kind=link}