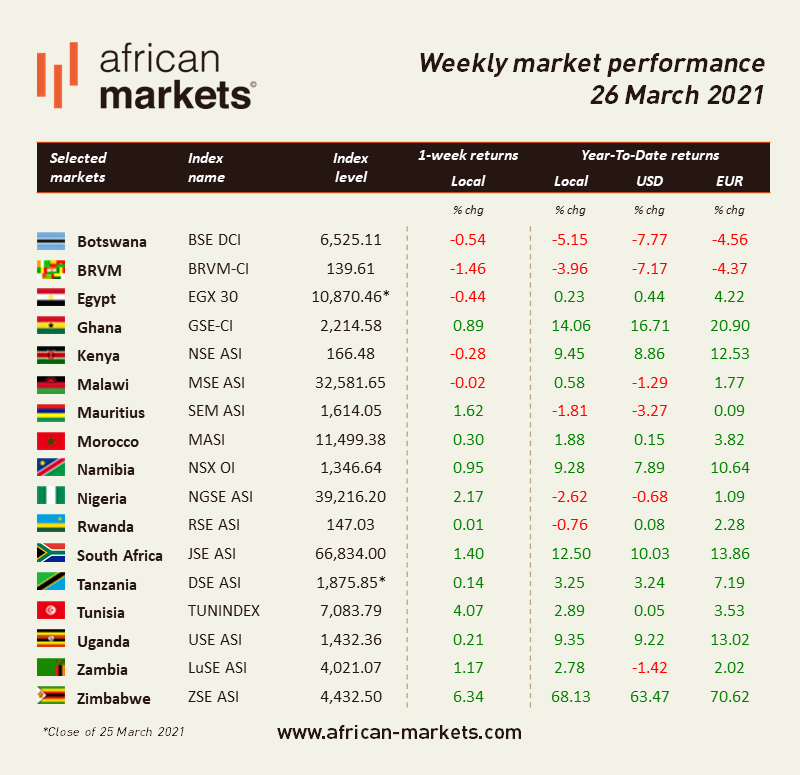

Overall sentiment on African equity markets was positive. Among the markets we cover, 12 of them advanced this week while 5 retreated. Zimbabwe led the pack as equities in Harare jumped 6.34%. Conversely, the BRVM was the laggard. Equities in Abidjan lost 1.46% over the 5-day period.

West Africa

BRVM – Bears were back on the Western Africa regional exchange pulling the benchmark index down during all five sessions of the week. Overall, the Composite Index retreated 1.46% and was back under the 140 points mark. Market activity rallied as XOF 562m (USD 1m) worth of shares changed hands every day on average. This is about 4 times the daily average turnover seen the week before.

The market is now down 3.96% year-to-date and the total market capitalization stands at XOF 4,201bn (USD 7.5bn). CFAO Motors is the top performer this week. The stock of the vehicle distributor jumped 10.26% over the 5-day period and is now up 19.44% since the start of the year. The market heavyweight, Sonatel, closed the week at XOF 12,500, down 3.84% over the week. Shares in the telecom operator are down 7.41% year-to-date.

NGSE – Bulls helped break the seven-week losing streak in Lagos. The benchmark index of the Nigerian stock exchange rallied 2.17% WoW closing on Friday at 39,216.20. Stocks are now down 2.62% YTD. Activity remained strong this week as NGN 4.3bn (USD 11.22m) worth of shares was traded on average over the last five days. The total market capitalization stands at NGN 20.5tn (USD 54.0bn).

The top performer this week is Stanbic IBTC. Shares in the banking group jumped 30% as management announced a 10.9% profit growth on Wednesday, along with dividend and bonus shares. The counter is now up 18.05% YTD. Dangote Cement, on the other hand, closed at NGN 225 (+2.27% WoW). The shares in the cement producer are down 8.13% YTD.

North Africa

BVC – Morrocan equities advanced this week. The MASI gained 0.30% in a week that saw MAD 170m (USD 18.9m) worth of shares change hands every day on average, lifted by a large operation on BCP’s shares on Friday. Total market capitalization stands at MAD 595bn (USD 65.8bn), up 1.88% YTD.

Notable performers this week include Sothema. The shares in the pharmaceuticals company soared 10.17% as it announced a 4.54% net profit growth along with a dividend. The counter is now up 50.60% YTD. The heavyweight, Maroc Telecom, closed at MAD 139 on Friday. The stock is down 4.14% YTD.

EGX – The Egyptian market declined further this week. The EGX 30 shed 0.44% and closed at 10,870.46 points on Thursday. Compared to the previous week, average daily turnover further dropped 4% to EGP 0.93bn (USD 59.5m) and the total market capitalization amounts to EGP 651.6bn (USD 41.5bn). The benchmark index is up 0.23% so far this year. Ismailia Development and Real Estate Co is a notable performer this week.

The stocks of the $100m market cap real estate developer jumped 8.74% over the week and are up 16.76% YTD. The Egyptian heavyweight, CIB, closed at EGP 60.9 on Thursday, up 2.89% YTD. Note that Fawry, the listed fintech company, closed lower on Thursday at EGP 34.89, down 0.23% from last week. The counter is still up 4.09% YTD.

East Africa

NSE – Kenyan equities cooled down this week as the Nairobi Securities Exchange’s benchmark index shed 0.28% WoW. However, the average daily turnover increased 21% to KES 482m (USD 4.4m) and the total market capitalization amounts to KES 2,558bn (USD 23.3bn). The market is up 9.45% YTD.

Standard Chartered is among the top performers this week. The shares in the banking group jumped 9.02% WoW as it decided to maintain its dividend despite posting decade-low profits in 2020. The counter is now up 0.52% YTD. Safaricom advanced this week as shares in the telecom operator closed at KES 38.75 on Friday, up 0.39% WoW. The counter is now up 13.14% so far this year.

Southern Africa

JSE – South African equities rallied towards the end of this week helping the JSE ASI advance 1.40% WoW and close at 66,834. The JSE tracked firmer global markets as better-than-expected economic data lifted sentiment, which has been dragged down in the past few days by concerns over new lockdown restrictions amid rising Covid-19 infections in parts of the world. South African equities are now up 12.50% so far this year. The JSE heavyweight, Prosus, closed at ZAR 1,669.14 on Friday (+2.09% WoW). It is now up 3.92% YTD.

ZSE – Bulls were back in Harare. The ASI rallied 6.34%. Daily average turnover significantly increased to around ZWL 93m (USD 1.1m) from ZWL 66m the week before. Total market capitalization amounts to ZWL 522bn (USD 6.2bn), up 68.13% so far this year.

{kind=link}