Financial systems of Caucasus, Central Asia are particularly vulnerable to shocks

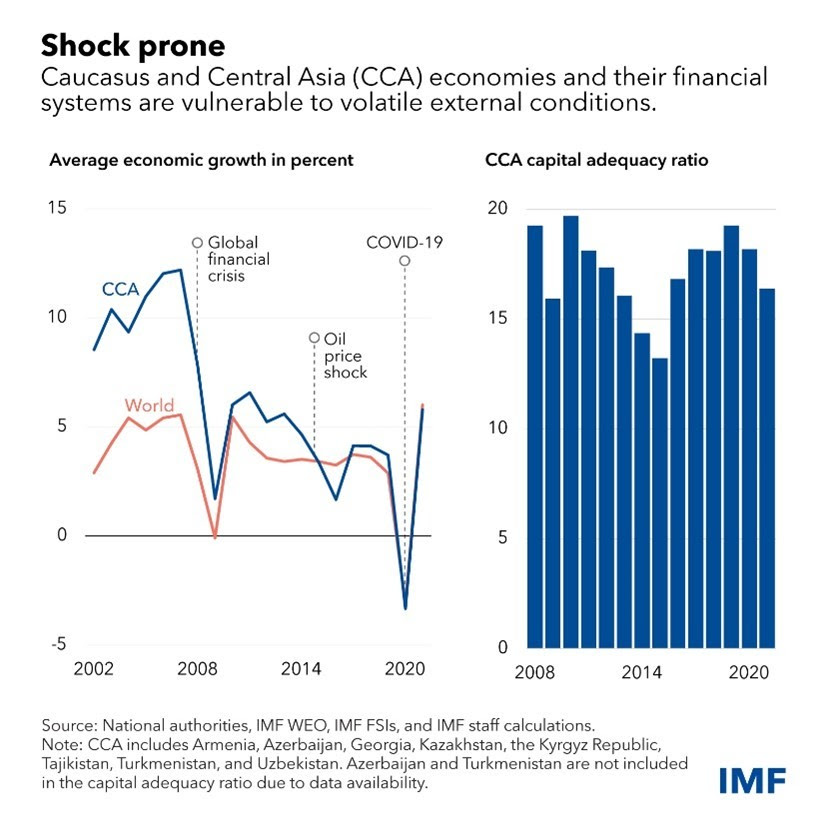

Heavily reliant on commodity exports, remittances and tourism, the economies of the Caucasus and Central Asia and their financial systems are vulnerable to volatile external shocks.

The Chart of the Week shows how exposed countries in the region are to such disruptions, which in the past have caused economic downturns and financial distress. Although the situation remains uncertain, the ongoing pandemic and the conflict in Ukraine could also have a substantial impact.

The CCA region’s financial systems are particularly vulnerable to the impact of external shocks on economic activity. At times, favorable external conditions have spurred large credit expansions and raised systemic risks. These booms have sometimes been followed by busts.

Indeed, adverse external shocks, such as the global financial crisis and the 2014-15 oil price shock, led to sharp contractions in credit and asset prices, which created a legacy of problem loans and resulted in costly public interventions to bail out banks.

Read: Ghana must have a decentralised regulatory framework for fintechs

Several features of regional banking systems have amplified these vulnerabilities. First, dollarization in CCA economies is well above emerging market peers. Second, banking sectors are small, concentrated, and often largely state-owned. Finally, gaps in banking regulation and supervision also contributed to the weak quality of bank loan portfolios and capitalization.

The pandemic has hit CCA economies hard in the past two years, but its impact on financial sectors has remained limited, helped by emergency measures to support households, businesses, and banks. However, the COVID shock is now compounded by the implications of international sanctions imposed on Russia, a country with sizable economic and financial linkages with CCA countries.

Looking ahead, stronger macroprudential policy frameworks will help increase financial sector resilience and mitigate the impact of large financial cycles and external shocks in CCA countries.

As experience in a few of these countries already shows, strong macroprudential policy frameworks have a key role in moderating credit and asset price booms, building larger buffers in bank balance sheets against adverse shocks, and reducing risks from common exposures and interlinkages between financial institutions.

Enhanced regulatory and legal frameworks for bank resolution and insolvency would also limit risks to financial stability and the public sector. Finally, reforms that reduce the role of state and promote competition would support greater financial inclusion and more sustainable credit and economic growth.

{kind=link}