What Ethiopia’s wheat revolution can teach Ghana about winning the tomato self-sufficiency battle

There are moments in a nation’s agricultural history when crisis and opportunity occupy the same breath. Ghana is in such a moment. Burkina Faso’s formalisation of a fresh tomato export ban on 16 March 2026 did not merely cause a market disruption; it exposed, with uncomfortable precision, a structural dependency that has persisted for decades. Ghana produces approximately 368,000 to 420,000 metric tonnes of tomatoes annually against a national demand of roughly 800,000 metric tonnes. The resulting shortfall of nearly 300,000 metric tonnes has historically been plugged by imports predominantly from Burkina Faso, at a cost to the Ghanaian economy of approximately GH¢760 million per year in fresh tomatoes alone, and an additional $54.4 million annually in tomato paste. In aggregate terms, inefficiencies across the tomato value chain are estimated to cost the country up to GH¢5.7 billion in unrealised economic value each year. These are not the figures of a sector in transition. They are the figures of a sector in structural neglect.

Yet on the other side of the continent, a comparable moment of reckoning rooted in chronic import dependence produced a significantly different response. Between 2016 and 2022, Ethiopia transformed itself from one of Africa’s largest wheat importers into a country that officially ceased government grain purchases abroad and began tentative exports. Cultivated wheat area rose from approximately 1.5 million hectares in 2016 to over 2.09 million hectares by 2022, with production climbing from 3.8 million tonnes to 6.23 million tonnes over the same period according to data from Ethiopia’s Central Statistical Agency and the USDA Foreign Agricultural Service. Average yields improved from 2.5 tonnes per hectare to nearly 3.0 tonnes per hectare. The government later reported output of 15.1 million tonnes in 2022/23 and 23 million tonnes in 2023/24, though independent analysts, citing FAOSTAT and USDA estimates that placed 2022/23 output closer to 5.8 million tonnes. Nevertheless, the directional trend is unambiguous. Ethiopia moved decisively on a staple crop deficit, and it moved through coordinated policy, not improvisation.

Ghana’s tomato sector currently achieves only 37% self-sufficiency, against an annual demand of 800,000 metric tonnes. Ethiopia’s wheat journey from 37% to near self-sufficiency took a decade of sustained, coordinated investment. Ghana has the tools, institutions, and now the political urgency to compress that timeline for tomatoes. |

The parallels between Ethiopia’s wheat position in 2015 and Ghana’s tomato position in 2026 are not incidental. Both involve a staple commodity with chronic production deficits; both are characterised by low average yields significantly below research-station potential; both depend on import flows whose security is ultimately beyond the host country’s control; and in both cases, the structural vulnerabilities were well-reported long before a crisis forced attention. The difference is that Ethiopia chose to act. The question before Ghana’s agribusiness policymakers, and before the current administration, is whether the Burkina Faso shock will be treated as an emergency to be managed or a turning point to be seized.

The Ethiopian template: What actually worked

A rigorous reading of Ethiopia’s wheat expansion suggests that it was not driven by a single intervention but by the simultaneous deployment of at least five reinforcing mechanisms, each of which is directly instructive for Ghana’s tomato challenge.

- Ethiopia’s wheat gains were disproportionately driven by the expansion of dry-season irrigated cultivation. Government-subsidised irrigation schemes in the Awash and Tekeze basins, combined with the deployment of gravity-fed canals and diesel-pump technology, effectively added a second crop cycle. In Ghana, the structural equivalent is stark. Tomato output is concentrated between June and November, leaving the dry-season months entirely without meaningful domestic supply. It is precisely this seasonal void that creates the import dependency Burkina Faso has historically filled. President Mahama’s announcement of a 60-hectare irrigation facility dedicated to year-round tomato production is therefore the correct strategic instinct, but the scale is grossly insufficient. Ghana’s Ministry of Food and Agriculture has set a target of 40,000 hectares under production by the end of 2026. Bridging that hectarage through rain-fed cultivation alone will not achieve year-round supply. Irrigation is not a supplementary instrument; it is the primary enabler of seasonal reliability.

- Ethiopia’s average wheat yield before the expansion sat at approximately 2.4 tonnes per hectare, below research-station potential. The state’s large-scale distribution of improved, rust-resistant bread-wheat varieties through the Ethiopian Grain Trade Enterprise, combined with extension training on planting dates and fertilisation, raised national average yields to nearly 3.0 tonnes per hectare within five years. For Ghana’s tomato sector, the productivity ceiling is equally defining. The national average yield of 8 tonnes per hectare compares unfavourably to Morocco’s 93 tonnes per hectare and even to Burkina Faso’s 18 tonnes per hectare. In the Upper East Region, which is Ghana’s principal dry-season tomato belt, the ILO’s scoping work has recorded yields as low as 1.5 to 2.0 tonnes per hectare, a fraction of the MOFA’s national average. The primary cause is seed quality, open-pollinated varieties extracted by farmers achieve limited yields, and imported hybrid seeds realise only approximately 25% of their listed yield potential under Ghanaian field conditions.

The Agriculture Minister’s announcement before Parliament on 25 March 2026 that resources have been allocated to a research project targeting 20 tonnes per hectare in partnership with WACCI and multiple research institutes is therefore one of the most consequential commitments the current administration has made. If Ghana can close even half the gap between 8 and 20 tonnes per hectare on the current 47,000 hectares, the production lift would be transformational. The critical requirement, as Ethiopia’s experience demonstrates, is that improved varieties must be domesticated through locally adapted seed systems, not reliant on continuous imports of hybrid seed that fail to express their genetic potential in Ghanaian soil and climatic conditions.

- Ethiopia’s use of fertiliser subsidies and machinery rental centres was neither universal nor indefinite. Input support was targeted at cluster-farming schemes and tied to the adoption of improved varieties, creating a package rather than an isolated transfer. The result was a simultaneous shift in both productivity and planted area. Ghana’s PFJ 2.0 programme has already established the institutional architecture for such targeted support, and the Mahama administration’s decision to supply farm inputs at no cost for the 2026 farming season removes a critical access barrier for smallholders in a year when global input prices are being pushed higher by the US-Israel-Iran conflict and its associated oil price shock. The risk, however, is the one Ethiopia also encountered; subsidy provision without a guaranteed off-take market creates production without commercialisation. Input support must therefore be structurally linked to verified buyer arrangements, whether through the National Buffer Stock Company, Ghana Comnmodity Exchange, institutional procurement, or contracted agro-processing relationships.

- Ethiopia’s milling sector, with a combined installed capacity of approximately 4 to 5 million tonnes per year, was chronically underutilised even as output grew, because working capital constraints and logistical gaps prevented the physical movement of grain to mills. In Ghana, the post-harvest failure is even more acute. The Chamber of Agribusiness Ghana estimates that approximately GH¢250 million worth of locally produced tomatoes rots annually due to the absence of cold storage, representing approximately 45% of domestic production. This is not a productivity failure; it is an infrastructure failure. No volume of improved seed or irrigation investment will generate sustainable commercial returns if 45% of output is lost before it reaches a market. The World Bank’s commitment of US$20 million channelled through the Dutch Ministry of Foreign Affairs to support Ghana in managing tomato supply disruptions, with a focus on storage capacity and supply chain strengthening, is therefore precisely the right application of external financing.

Ethiopia’s experience teaches that post-harvest infrastructure is not downstream of the production challenge; it is co-equal to it. In Ghana, where roughly 45% of domestically produced tomatoes are lost annually to the absence of cold chain and processing capacity, infrastructure investment is a prerequisite for the productivity gains sought through seed improvement and irrigation. |

- Ethiopia’s wheat expansion was organised around explicit political commitment at the highest level, multi-agency coordination, and measurable targets. The Ethiopian Grain Trade Enterprise served as the operational backbone, coordinating seed multiplication, input delivery, and government procurement. Ghana has a credible equivalent in the inter-ministerial architecture being assembled around its National Tomato Emergency Strategy, which the Chamber of Agribusiness Ghana has articulated as a seven-phase, 12-month roadmap anchored by a Presidential declaration, an inter-ministerial committee, and an allocation of GH¢430 million in the 2026 Supplementary Budget. This architecture is appropriate. What will determine its effectiveness is not the quality of the plan on paper but the discipline of execution against the plan.

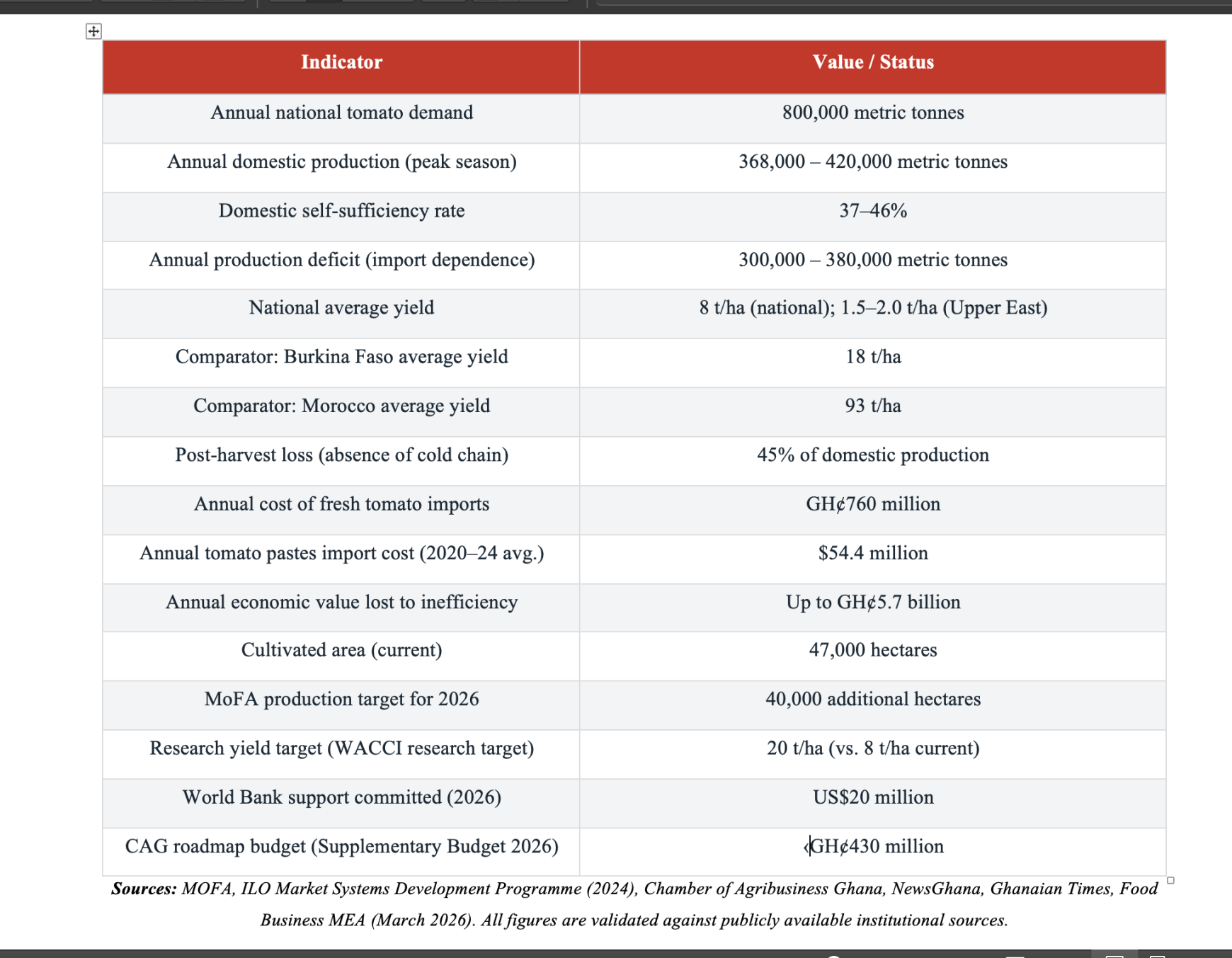

Ghana’s tomato sector: The data behind the crisis

It is important to ground the policy discussion in the actual numbers, because the scale of Ghana’s tomato deficit is frequently understated in public discourse. The table below sets out the key production, demand, and market parameters.

What the table makes clear is that Ghana’s tomato challenge is simultaneously a yield challenge, an infrastructure challenge, a seasonal supply challenge, and a market coordination challenge. No single intervention resolves it. Ethiopia’s experience is instructive precisely because the Ethiopian state did not pick one lever; it pulled all of them concurrently, aligned behind a single commodity target, under sustained political authority.

From wheat fields to tomato farms: A policy roadmap for Ghana

Drawing on the Ethiopian model and calibrated to Ghana’s specific institutional context, the following recommendations represent the five strategic priorities that an agribusiness advisory perspective would advance for the current administration.

- The gap between yield potential and field performance is a seed systems failure. Ghana cannot achieve 15 to 20 tonnes per hectare on imported hybrid seed that expresses only 25% of its potential under local conditions. The research partnership between MOFA, WACCI, and Ghana’s research institutes must produce locally adapted, high-performing open-pollinated or F1 hybrid varieties that are multiplied domestically and available through a certified seed system. Institutions such as CSIR-Crops Research Institute at Fumesua, CSIR-Savanna Agricultural Research Institute (SARI), and the West African Centre for Crop Improvement (WACCI) at the University of Ghana should be resourced to lead this domestication. ILO’s Market Systems Development programme has already demonstrated the feasibility of local seed commercialisation through Agri-Commercial Seed Services Limited. That model should be scaled, not replicated from scratch.

- Seasonal supply concentration is the root cause of import dependency. A country that does not produce tomatoes between December and May will always require external supply to cover that period, regardless of how productive the June to November season becomes. The government’s 60-hectare irrigation announcement is a statement of intent; it needs to be followed by an irrigation masterplan that maps the dry-season production potential of the Volta Basin, the White Volta corridor, and the key reservoir-fed schemes at Dawhenya and Akumadan. Rehabilitation of these existing schemes should precede the development of new infrastructure. Solar-powered drip irrigation, which has transformed dry-season horticulture productivity in parts of northern Ghana, should be incorporated into the mechanisation and irrigation programme of PFJ 2.0, specifically for tomato.

- It would be a serious strategic error to rapidly expand tomato cultivated area to 40,000 hectares without first substantially reducing the 45% post-harvest loss rate. If production doubles whilst losses remain at 45%, the net gain in marketed supply is modest and the economic loss to farmers is amplified. The US$20 million World Bank-facilitated support package should be directed primarily at modular cold storage units at aggregation points in the major producing districts of Brong, Ahafo, Greater Accra (Dawhenya), and the Upper East. Simultaneously, the government should provide tax incentives or concessional credit to private agro-processors including the existing tomato paste manufacturers to expand processing capacity, specifically targeting the seasonal surplus that currently rots in the field. A well-capitalised processing sector transforms a perishable surplus problem into a strategic stockpile advantage.

- Ethiopia’s government procurement system, which offered farmers guaranteed off-take at predictable prices, was as important as the seed distribution programme in persuading smallholders to commit land and labour to wheat. Ghana’s National Buffer Stock Company has been allocated GH¢3 million to purchase locally produced crops, a meaningful signal, but insufficient at the scale required. The institutional mechanism that Ghana needs is a formal tomato procurement scheme, perhaps structured as a seasonal forward contract through NAFCO or the Buffer Stock Company, guaranteeing dry-season tomato producers a minimum price. This reduces farmer risk, crowds in private agribusiness investment in contract farming, and incentivises dry-season production in irrigated areas where the infrastructure cost is highest and the payoff period longest.

- Ethiopia’s most serious long-term vulnerability is not climatic or technical; it is statistical. The contested production figures of 2023 and 2024 where official government claims of 15 to 23 million tonnes diverge from independent estimates of 5 to 7 million tonnes have undermined investor confidence, distorted import planning by millers, and created a policy environment in which it is impossible to assess whether interventions are working. Ghana must not replicate this error. MOFA, GSS, and the Chamber of Agribusiness Ghana should jointly establish a tomato sector monitoring framework with independently verified, quarterly production and market data, covering cultivated area, yield, post-harvest loss rates, processed volume, import volume, and consumer prices across major markets. Reliable data is not a bureaucratic add-on to an agribusiness programme; it is the feedback loop through which the programme learns and corrects itself.

Why this matters now

It would be analytically incomplete to discuss Ghana’s tomato self-sufficiency ambition without situating it in the current macroeconomic environment. The US-Israel-Iran conflict, which intensified from late February 2026, has pushed Brent crude prices from approximately $70 per barrel to over $82 per barrel within days, a 10 to 13% increase. For Ghana, an economy that imports over 80% of its fuel in refined form against an oil-related import bill of US$5.1 billion in 2025, this is not a distant geopolitical event. It is a direct fiscal and foreign exchange exposure. The cedi has already depreciated 4.8% since the start of 2026, the sharpest decline among 23 African currencies tracked by Bloomberg. Higher energy costs will push up transport, irrigation fuel, and cold chain operating costs across the agricultural value chain, whilst cedi depreciation will make imported fertiliser and agrochemicals of which Ghana imports over 70% of its requirements more expensive in local currency terms.

This macroeconomic context strengthens, rather than weakens, the case for the domestic tomato production drive. Every percentage point of import substitution that Ghana achieves in its tomato sector reduces the foreign exchange drain on its current account, reduces the import-inflation transmission channel through which global commodity shocks reach Ghanaian consumers, and reduces the fiscal pressure on a government already managing a delicate IMF programme. Tomato self-sufficiency is not an agricultural target alone; it is a macroeconomic resilience strategy too.

The Burkina Faso tomato ban (subsequent ban lift) and Iran conflict’s oil price shock are not unrelated events in Ghana’s economic landscape. Both expose the same structural vulnerability. An economy whose food and energy security depends disproportionately on external sources beyond its control. Addressing the tomato deficit is therefore both an agricultural imperative and a macroeconomic stabilisation strategy. |

The opportunity in the crisis

Ethiopia did not solve its wheat deficit in a single season. It built a system, imperfect, contested in its statistics, and still reliant on imports in the private sector even as government claims self-sufficiency but a system nonetheless, one that demonstrably moved average yields, expanded cultivated area, and reduced official import dependence over a decade of sustained political commitment and institutional investment. Ghana’s Feed Ghana and Adwumawura framework, the National Tomato Emergency Strategy, the World Bank financing, seed research partnership, and President Mahama’s irrigation announcement together constitute the institutional scaffolding for an equivalent transformation in the tomato value chian. What they do not yet constitute is a coordinated system.

The transition from scaffolding to system requires two things that are available to Ghana right now. The political will to hold ministries accountable to specific, time-bound, and independently monitored targets; and the agribusiness intelligence to sequence investments correctly, prioritising post-harvest infrastructure alongside, not after, production expansion, and building the seed systems that will make irrigation investment economically viable. Ethiopia’s lesson, properly read, is not that Africa can achieve food self-sufficiency through government mobilisation alone. It is that coordinated, data-driven, private sector-partnered investment in the right sequence can compress decades of agricultural stagnation into years of measurable progress.

Ghana’s tomato farmers grow a vegetable that feeds the nation, generates employment across the value chain, and represents a straightforward path to import substitution, foreign exchange conservation, and food security. They deserve, and Ghana’s macroeconomic stability now requires, a policy environment as serious as the challenge they face.

{kind=link}